If you’re one of those who prefer to put off tax-saving until the last minute, welcome to the club! Let’s turn that procrastination into profit. With only 10 days left, it’s time to get your tax-saving game face on. Remember, every rupee saved is a rupee earned. Explore tax-saving options like tax saving mutual funds, EPF, PPF, HRA and health insurance to not only reduce your tax burden but also grow your wealth. It’s a win-win situation!

ELSS: Tax Saving Mutual Funds (80C)

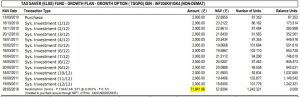

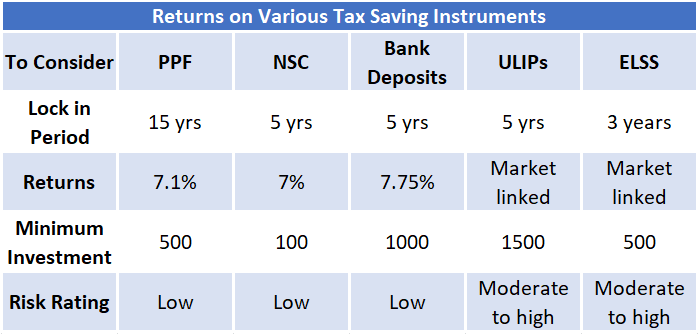

One of the most popular tax-saving options is ELSS, or Equity-Linked Saving Schemes, which are mutual funds that primarily invest in equity markets. ELSS has the shortest lock-in period and provides the highest returns among all tax-saving options. If you harvest it smartly, you can even escape long-term capital gains (LTCG) tax of 10 percent on redemptions of more than 1 Lakh in a year.

Public Provident Fund (80C)

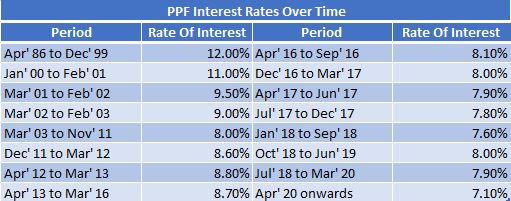

PPF is a reliable and safe long-term savings-cum-investment product that offers attractive returns, tax benefits, and a lock-in period of 15 years. However, it has an interest rate risk. For example, the interest rates on PPF have dropped from 12% in the 1990s to the current rate of 7.1% which means the returns can decrease if the interest rate falls. You may explore our detailed comparison of PPF and ELSS: Even Worst ELSS Outperforms PPF

EPF & other Fixed Income Options (80C)

Another tax-saving option is investing in the EPF (Employee Provident Fund) under Section 80C. EPF is a long-term investment option that can avail of tax benefits. The current rate of interest on an EPF account is 8.1% p.a., compounded annually, and the maturity amount is tax-free if you are in continuous service with the same employer for five years or more.If you are terminated or unemployed due to ill health, withdrawals will not attract tax. if you aren’t exhausting the 2.5 lakh limit then you may want to invest further through the Voluntary Provident Fund. To understand the intricacies of EPF and other fixed income options; Make Your Financial Plan Indestructible.

Health Insurance for Self and Family (80D)

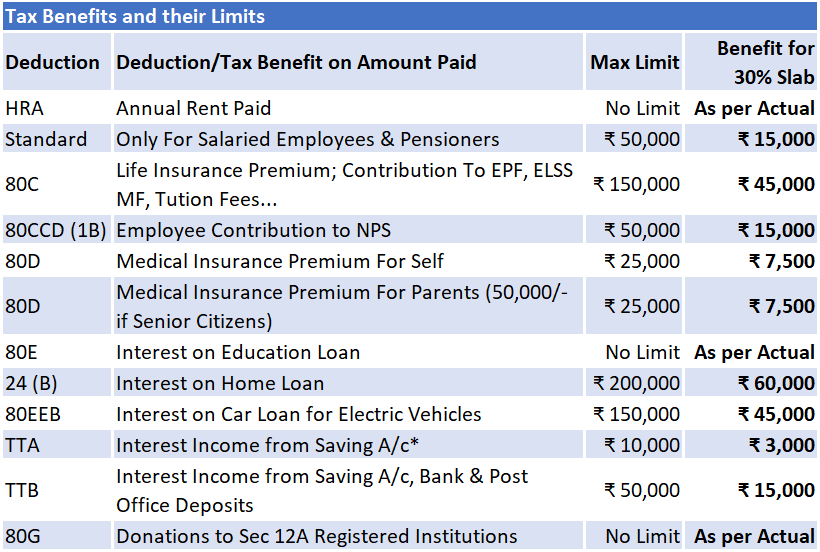

Health insurance is a bare necessity of life in a metro today. Under Section 80D, the government offers tax benefits for premiums paid towards health insurance policies at ₹25,000 for self, spouse, and dependent children and ₹50,000 for senior citizen parents. Spending on preventive healthcare is also eligible for deduction under Section 80D with a maximum cap of ₹5,000/- for self or family and ₹7,000/- for parents.

House Rent Allowance

HRA is a common component of employee compensation. employees who receive HRA as a part of their salary can claim tax benefits for the rent they pay. Suppose an employee earns a basic salary of Rs. 50,000 per month and pays a monthly rent of Rs. 15,000. If the employer provides an HRA of Rs. 20,000 per month, then the employee can claim exemption on the following:

Actual HRA received: Rs. 20,000

Actual rent paid minus 10% of basic salary: Rs. 15,000 – (10% of Rs. 50,000 = Rs. 5,000) = Rs. 10,000

50% of basic salary: 50% of Rs. 50,000 = Rs. 25,000

The lowest amount, in this case, is Rs. 10,000, so the employee can claim an exemption on this amount and the remaining Rs. 10,000 of HRA will be taxable.

Add on bonus: It is possible to claim HRA benefit even if you do not stay in a rented place. You can pay rent to your parents or other relatives and claim tax benefits for the same. However, in such cases, your parents or relatives would need to show the rent received as income from property and pay tax on it. It is important to ensure that the rent payment and receipt is genuine and not done just for the purpose of tax evasion, as the tax authorities may investigate such cases.

Tax Deduction on Home Loan Interest (Sec 24B)

Homeowners can claim a deduction of up to 2 Lakhs on their home loan interest if the owner or his family resides in the residential property. The same treatment applies when the house is vacant. If you have rented out the property, the entire home loan interest is allowed as a deduction.

Structuring your Salary

You can incorporate tax-free components like leave travel allowance (LTA), meal coupons and gadget allowance in your salary structure. LTA is tax-free twice in a block of four years, while the annual allowance for meal coupons can be up to 26,400/- For gadgets and furniture provided by the employer, employees are taxed at only 10% of the value of these items.

In conclusion, tax planning is crucial for managing personal finances and achieving long-term financial goals. With the plethora of tax-saving options available, it’s easy to get confused. Let’s compare our options.

In conclusion, tax planning is crucial for managing personal finances and achieving long-term financial goals. With the plethora of tax-saving options available, it’s easy to get confused. Let’s compare our options.

Compared to other investment options with tax-saving benefits, ELSS or tax-saving mutual funds yield the highest returns and offer the shortest lock-in period for someone with the commensurate risk appetite. By investing in the right combination of these tax-saving options, individuals can reduce their tax liability and optimize their long-term wealth creation.