Hmmm, “30% to taxes?” Richa muttered, tapping away on her calculator. “There’s got to be a better way.

Richa, a savvy marketing professional in her early 30s, wasn’t just frustrated by the long hours she put in, she was frustrated with a significant chunk of her salary being taxed.

“Ugh, these taxes are killing me!” she grumbled to her friend Neha over coffee.

“I max out all the usual stuff like PF, LIC, ELSS funds, even got medical insurance 80D, NPS… still, I’m paying over ₹20,000 in taxes every month!”

Neha: “Have you thought about buying a house? Everyone says you can save a ton on taxes with a home loan!”

Richa’s eyes lit up. “Really? Could that be the magical solution to my tax woes?”

Richa’s mind raced. “Interesting! But what kind of savings are we talking about? And what are the terms of these home loans? I don’t want to jump into something bigger than I can handle.”

Before exploring home loan options, let’s understand the two key tax deductions associated with them.

- Section 80C: Offers a deduction of up to ₹1.5 lakh on the principal amount repaid each year. Since Richa already utilizes the full 80C limit with existing investments, this won’t bring any additional tax savings.

- Section 24(b): For self-occupied properties, this offers a maximum deduction of ₹2 lakh on the interest paid annually (this is the more impactful one).

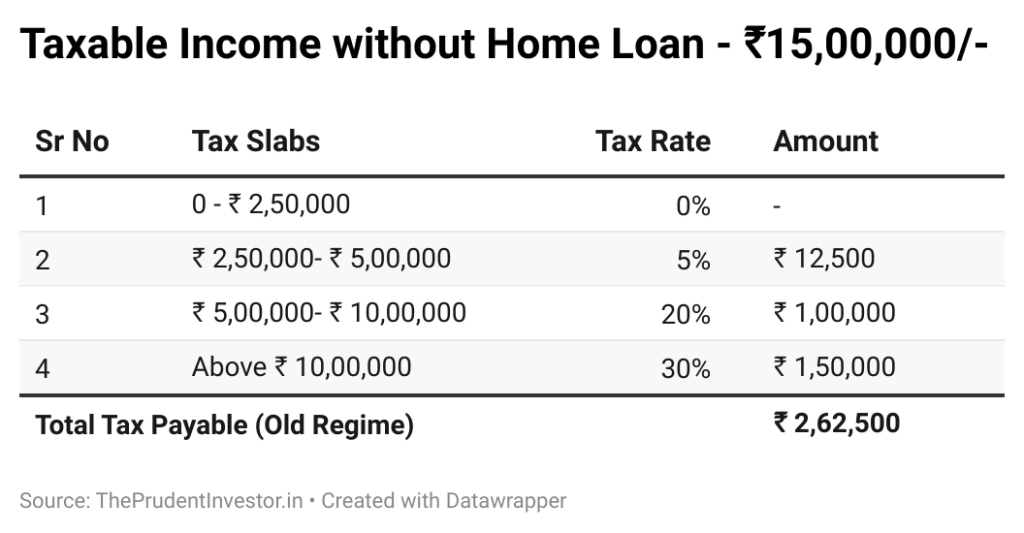

Richa’s Current Tax Situation:

Let’s take a snapshot of Richa’s current tax situation to compare it with the potential scenario after taking a home loan.

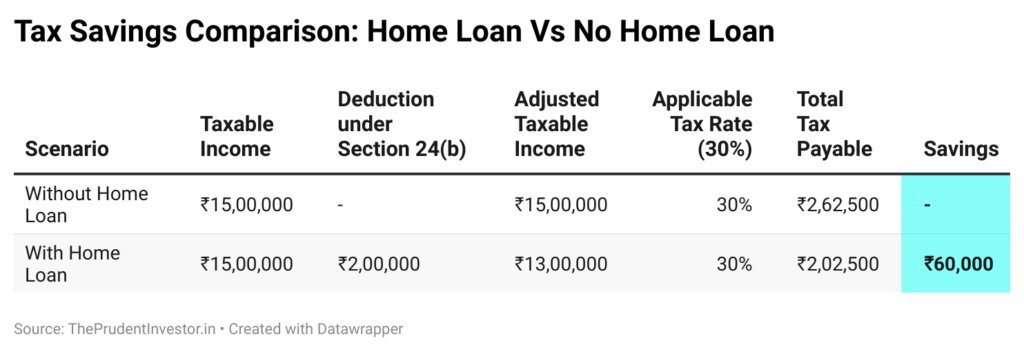

Richa’s current tax situation, as highlighted in the table, translates to an annual tax of ₹2,62,500, or roughly ₹21,875 per month. This sizable monthly deduction motivates her to explore potential solutions like home loans to reduce her tax liability.

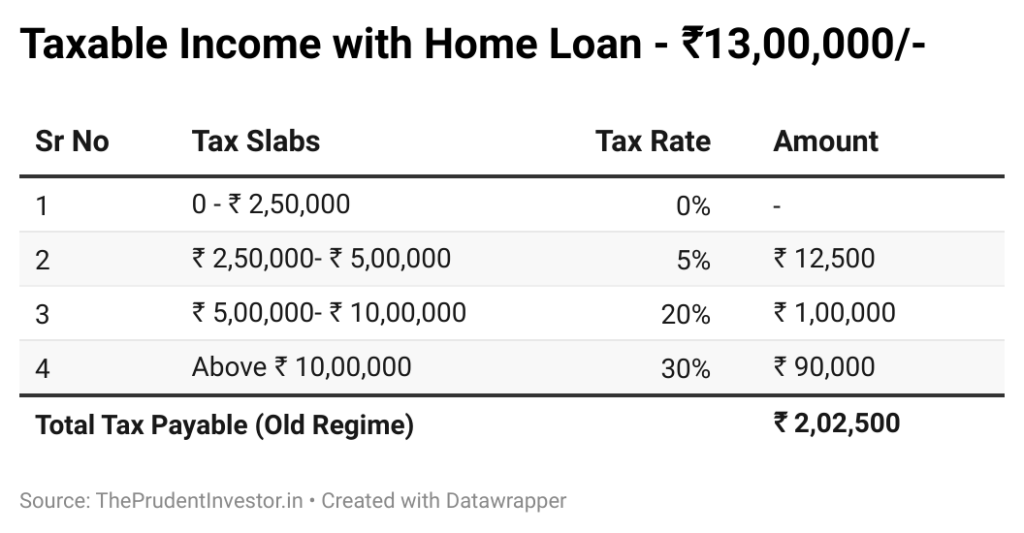

Simulating Richa’s Scenario with a Home Loan:

Imagine Richa takes a home loan of ₹50 lakh with an interest rate of 9%. she’d pay roughly ₹4.5 lakh in annual interest. This sounds significant, right?

Key Point: The maximum deduction under Section 24(b) is capped at ₹2 lakh, regardless of the actual interest paid. So, while Richa pays ₹4.5 lakh, she can only deduct ₹2 lakh from her taxable income.

This reduces her taxable income to ₹13 lakh (₹15 lakh – ₹2 lakh).

Quantifying the Actual Benefit:

Deduction ≠ Tax Savings: Even in the highest tax bracket, her actual savings will be 30% of ₹2 lakh, which translates to ₹60,000 per year or roughly ₹5,000 per month.

Comparing Scenarios:

Now that we’ve analyzed both options, let’s compare Richa’s current tax situation without a home loan to a hypothetical scenario with a home loan:

While Richa initially hoped for a significant tax reduction, a home loan might offer a benefit of around ₹5,000 per month.

It’s crucial to remember:

- Is owning a home your top financial priority? Don’t solely rely on tax benefits for such a major decision.

- Can you comfortably afford the monthly EMIs and additional expenses? Analyze your budget carefully.

Remember:

- If the loan is in joint names, both individuals can claim separate deductions under Section 80C and Section 24(b).

Do you think, is a home loan the right path to reduce your tax burden?