I recently met a school friend I hadn’t seen in years. Over coffee, we chatted about the things we used to dream about and the journeys we embarked on. As we talked about different things, we eventually started talking about money.

My friend, now a successful professional working for a multinational company, began discussing his investment choices.

“I only invest in Fixed Deposits, Provident Fund and Sukanya Samriddhi Yojana” he said confidently as if he’d found the secret to keeping his money safe. “They’re the safest,” he added.

His words got me thinking. In today’s ever-changing financial world, can you really count only on Fixed Deposits and Provident Funds to keep your money completely safe? Are they as perfect as they seem?

In India, there are a number of popular investment choices, but each one comes with its own set of risks. In this article, we will explore the hidden risks behind some of the most popular investment choices in India.

Fixed Deposits: The Illusion of Safety

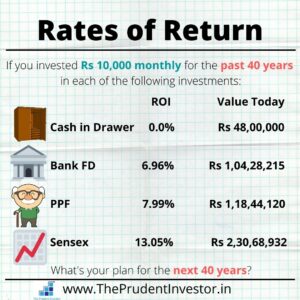

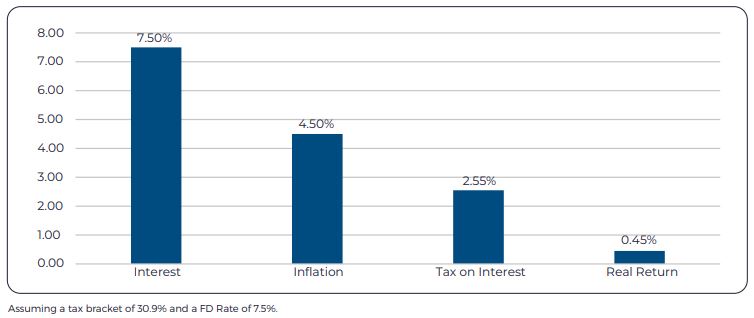

Fixed Deposits (FDs) have long been considered a safe haven for investors. They offer seemingly attractive returns, often hovering around 6-8%. However, these numbers don’t tell the whole story.

Inflation in India averages around 6%, and FD interest is subject to taxation. For individuals in the 30% tax bracket, the real return on FDs can dip into negative territory. This is a clear reminder that even seemingly secure investments have hidden risks.

Public Provident Fund: A History of Falling Returns

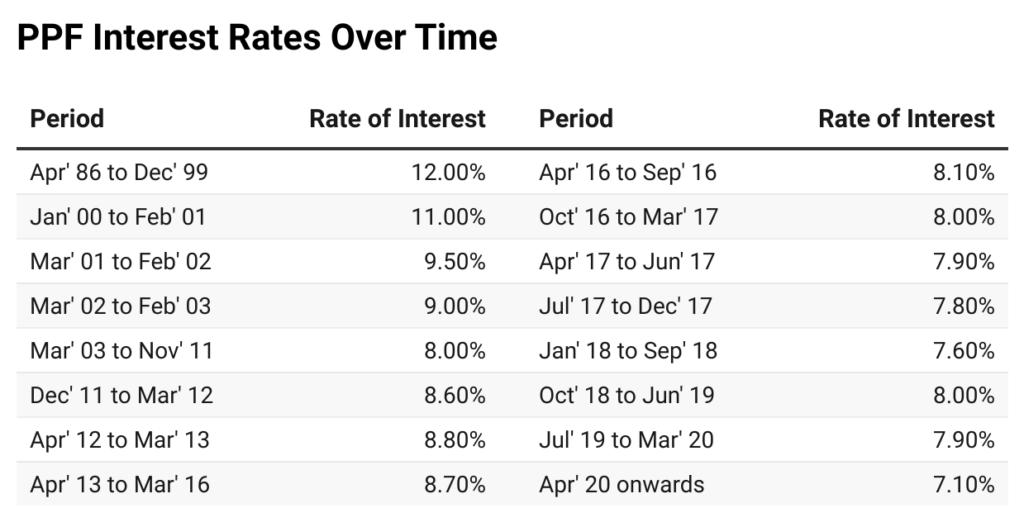

Public Provident Fund (PPF) is a popular investment option in India, known for its tax-free returns and government backing. However, it is important to remember that no investment is completely risk-free, and PPF is no exception.

One of the biggest risks associated with PPF is the risk of interest rate fluctuations. In the past, PPF offered double-digit returns, but interest rates have dwindled over the years, currently resting at 7.1%.

Gold: Glittering but Not Always Golden

Gold holds a special place in the hearts of many Indians, yet, its track record isn’t all sparkle and shine. While gold has managed to outpace inflation over the long haul, it’s crucial to understand that it has its moments of going up and down.

But wait, there’s more to this golden tale. When we talk about physical gold, it gets a bit more complicated.

- First, there’s the issue of purity – you want to make sure you’re getting the real deal.

- Then comes the practical stuff – storing it securely, which can cost you extra in the form of locker fees.

- And if you’re a fan of gold jewellery, there’s another twist – making charges. These extra expenses can nibble away at your returns, making gold lose some of its shine as an investment choice over time.

Real Estate: The Love Affair with Liquidity Risk

Real estate has long captured the hearts of Indian investors, but it comes with a unique set of risks. One of the biggest risks associated with real estate is liquidity risk. This means that it can be difficult to sell your property quickly if you need to raise cash.

Real estate doesn’t operate like a collection of separate items on a shelf. You can’t, for example, pick and sell just your balcony or kitchen, even if you only require a portion of the property’s value. When you decide to sell, it means putting the entire property on the market.

Additionally, it’s worth noting that the rental yield in the real estate market tends to be relatively low, and the prospects for capital appreciation can be somewhat erratic, as highlighted in this article – https://theprudentinvestor.in/indian-real-estate/

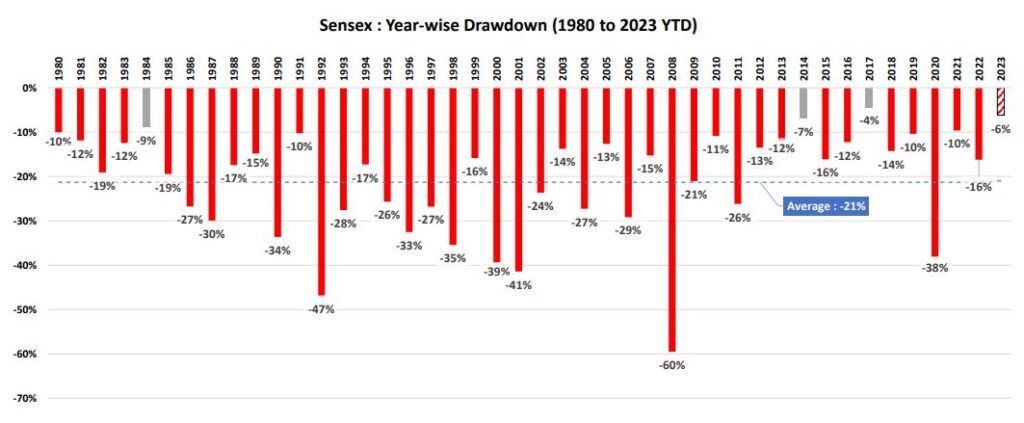

Indian Equity: Riding the Rollercoaster of Volatility Toward Long-Term Growth

Indian equity markets have the potential for substantial long-term growth. markets often experience periodic dips, with temporary declines ranging from 10% to 20% happening quite regularly. This volatility can rattle the nerves of investors who are hoping for a smooth ride with consistent returns.

But here’s the secret sauce: Equity investments are like planting a tree. You don’t expect it to bear fruit overnight, right? In the same way, you shouldn’t anticipate instant results from your equity investments. The key is to give them time to grow, just as you patiently wait for that tree to bear fruit.

So, if there are no risk-free investments, what should you do?

The key is to diversify your portfolio. This means investing in different asset classes, such as debt, equity, and gold. This way, if one asset class performs poorly, you will still have other assets to cushion the blow.

Many investors make the mistake of investing for the long term in debt products, such as FDs and PPFs. However, these products offer relatively low returns, and they can be eroded by inflation.

Imagine you’re going on a trip. You might ride your bicycle or walk if you’re going a short distance, like to a nearby park. But if you’re going on a really long journey, like from one city to another, you’d need something faster, like a car or an aeroplane, right?

No Fields Found.