Many people think that the key to getting rich is making a lot of money. Let’s find out.

Grace Groner was orphaned at 12 and was raised by kind neighbors. She later lived in a tiny one-bedroom cottage. She shopped at second-hand sales, loved to walk everywhere, and worked for most of her life as a secretary. So it was surprising to her alma mater, Lake Forest College, to learn that upon her death she left a gift of $7.2 million to the institution to start a scholarship program.

In 1935, at age 25, she got a job as a secretary at Abbott Pharmaceuticals. In her first year at Abbott, she bought three shares of Abbott stock for $180. After 75 years of stock splits and dividend reinvestments, she died with over 100,000 shares of Abbott stock.

Just Lay a Brick

The phrase “Rome wasn’t built in a day” is typically used to remind someone of the time needed to accomplish something great.

It does take time — sometimes years — to master a skill, craft, or habit. Though it’s good to keep your dreams in perspective, it’s also vital to remember that:

Rome wasn’t built in a day, but they were laying bricks every hour.

The problem is that it can be really easy to overestimate the importance of building your Roman empire and underestimate the importance of laying another brick.

It’s just another brick. How much of a difference does it make? More important to focus on the dream of Rome. Right?

Actually Rome is just the result, the bricks are the system. The system is greater than the goal. Focusing on your habits is more important than worrying about your outcomes.

We all seek investment performance that is above average, but how do we achieve that?

In October 1990, Howard Marks discussed the formula of a major mid-West pension plan which delivered returns over fourteen years that had been way ahead of the S&P 500. The director shared what he considered the key:

“We have never had a year below the 47th percentile over that period or, until 1990, above the 27th percentile. As a result, we are in the fourth percentile for the fourteen-year period as a whole. What the pension fund’s record tells me is that, in investments, if you can avoid losers (and losing years), the winners will take care of themselves.”

The best foundation for above-average long-term performance is the absence of disasters. In the long run, seeking relative performance which is just a little bit above average consistently – with protection against poor absolute results in tough times – will yield higher returns than “trying to hit sixes.”

We Only Need To Cross The Finish Line

Investing isn’t about achieving perfectionism. Our ultimate goal isn’t to be the best or to finish first. Our goal is just to finish. A participation trophy is good enough.

That’s where good enough comes into play. All we need is an investing strategy that is good enough to get us to the finish line.

The idea that investing only requires us to do good enough is difficult to digest. We have been taught our entire lives that it’s not just about being good enough – it’s about being the best. And if not being the best overall, at least being the best we can be.

Here is the funny thing about investing. You don’t have to be the best. You don’t even have to be the best that you can be. You just have to be decidedly average.

How Can We Implement This With Our Investments?

- A simple plan, executed over a long period of time, usually beats a complicated plan, that is modified constantly. Although Grace held just one stock. What matters is that she diligently stuck with the plan over many decades.

- Grace held onto her stock through 13 recessions, and many other corrections, wars and difficult economic times, that may have shaken out many more sophisticated investors. She did not trade her stock, try to time the market, sell it after a year of bad earnings or get scared by negative market experts. She looked at the big picture so time richly rewarded her. There’s no surer way to mess up your investment returns than to freak out when things are looking bad. No one can predict the future. Markets will rise and fall. If you freak out when things look bad, you’ll inevitably miss the climbs that come later.

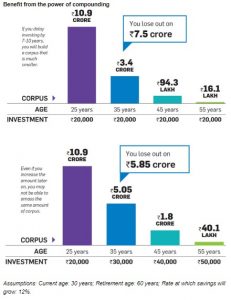

3. Investing from an early age can make a huge difference in eventual results. If Grace had invested $180 in 1945 instead of 1935, she would have left behind $1.7 million, instead of $7.2 million. Time is a powerful leveraging tool. We can’t predict what will happen in the short term. But we can safely assume that if companies keep growing and innovating, the markets will deliver in the long term.

4. Invest As Much As You Can. This may be the most important thing you can control. Many investors think about rates of return. What they can do to get the highest rate of return on their investments.

But doubling a small amount of money is still a small amount of money. To get to the finish line, we ultimately have to brute force save as much money as we can so that our returns actually amount to something.

Good enough investing is what we’re looking to do. Pick a reasonable asset allocation and stick to it.

How many investors can stay the course over decades? The investor’s prime challenge is to fight the urge to de-risk in a bear market and add risk in a bull market. Many will win this battle; some will win the war. Will you?