Imagine receiving an email from your employer offering health insurance for your parents. Sounds great, right? Unfortunately, the excitement can quickly fade when you realize that you have to bear the premium cost for their coverage.

Additionally, the offered ₹5 lakh coverage might not be sufficient for major medical procedures in today’s world of rising medical costs. This raises a crucial question: do the health plans offered by companies provide adequate coverage?

Let’s take Raj’s example. His company offered ₹5 lakh coverage for his parents with two options:

- Copay (20%): He would pay 20% of the claim amount (meaning a portion of the bill out of his pocket), and the insurance company would cover the remaining 80%. The annual premium for this option was around ₹30,000.

- No copay: This option eliminated the copay, but the annual premium jumped to ₹70,000, raising concerns about affordability.

While the no-copay option seemed appealing, the higher premium was a major hurdle. However, the copay option also had its drawbacks. For instance, if Raj’s parents faced a hospitalization bill of ₹5 lakh, the copay would translate to ₹1 lakh out-of-pocket expense, which could be significant for major procedures.

Given these options, Raj explored other avenues. He considered a personal health insurance policy but ultimately opted for the company-provided plan due to its advantages:

- No pre-medical checkup: Unlike individual plans, company plans often waive pre-medical checkups for dependents, especially when they are young and healthy.

- Waiver of waiting periods: Pre-existing conditions are usually covered immediately, unlike individual plans which may have waiting periods.

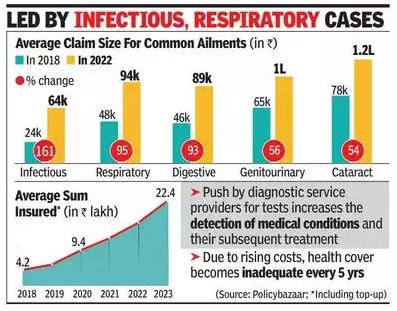

However, it’s crucial to remember that the offered ₹5 lakh coverage might not be sufficient considering the rising medical inflation, doubling every 5 years according to sources like Times Of India.

Fortunately, there are solutions to bridge the gap between affordability and adequate coverage. One such solution is a super top-up health insurance policy.

Introducing Super Top-up Plans: Supercharge Your Coverage

Think of a super top-up plan as a safety net that kicks in only after your existing plan (in this case, the company plan) reaches its limit. This allows you to increase your overall coverage at a more affordable cost compared to significantly increasing the base plan coverage.

Here’s how super top-up works:

Example: Say Raj opts for a super top-up plan of ₹10 lakh with a deductible of ₹5 lakh. This means the super top-up only starts paying after the expenses exceed the initial ₹5 lakh covered by the company plan.

Scenario: If Raj faces hospital bills of ₹8 lakh, the company plan would cover the first ₹5 lakh. The remaining ₹3 lakh would be covered by the super top-up plan, ensuring comprehensive financial protection.

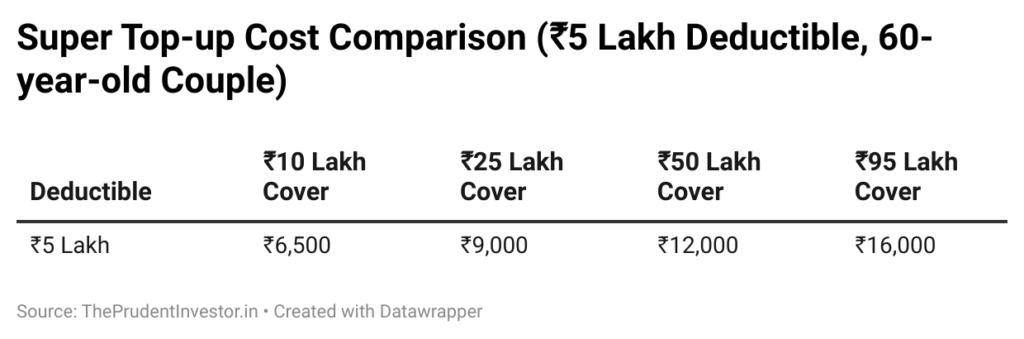

For instance, a super top-up plan offering ₹10 lakh coverage with a ₹5 lakh deductible might cost approximately ₹6,500 annually for a 60-year-old couple.

The table below provides a sample of how the annual cost can vary based on the chosen coverage amount, keeping the deductible constant at ₹5 lakh:

Benefits of Super Top-up Plans:

- Increased Coverage: They provide additional protection against rising medical costs.

- Cost-effective: Compared to increasing base plan coverage significantly, super top-up plans offer a more affordable solution for extending coverage.

Keep in mind some limitations:

- Room rent restrictions: Some plans have lower room rent limits compared to regular health insurance.

- Dual claim process: Managing claims might involve navigating both the company plan and the super top-up plan.

- Waiting periods: Super top-up plans, like other health insurance policies, might have waiting periods for pre-existing conditions.

Building a robust healthcare safety net for your family requires striking a balance between cost and coverage. While company-offered health insurance has advantages, consider supplementing it with a super top-up plan to address the limitations in today’s healthcare landscape.

How much health cover do you have? Consider if a Super Top-up plan can bridge the gap!

For further reading – https://theprudentinvestor.in/health/