Imagine you’re standing on the starting block of the Olympic pool, ready to race for gold. The crowd is cheering, your heart is pounding, and you’re focused on the finish line. You’ve trained for years for this moment, and you’re ready to give it your all.

But then, something unexpected happens. Your goggles fill with water, and you can’t see anything. What would you do?

What-If Scenarios: A Training Technique for Athletes

Michael Phelps, the most decorated Olympian of all time, was faced with this exact challenge during the 200-meter butterfly final at the 2008 Beijing Olympics. In the middle of the race, his goggles filled with water, and he was essentially swimming blind.

But Phelps didn’t panic. He remained calm and collected, and he relied on a training technique called “what-if scenarios.”

What-if scenarios are hypothetical situations that athletes can use to prepare for anything. For example, Phelps’ coach, Bob Bowman, once deliberately cracked his goggles before a local race to prepare him for the unexpected.

Phelps didn’t notice his goggles were broken until he dived into the pool and they suddenly began to fill with water. But he didn’t let this malfunction stop him. Instead, he counted his strokes, a strategy he and Bowman had developed in training to determine precisely how many strokes it took to complete a length of the pool.

When this scenario played out again during one of the biggest races of his career, the 200-meter butterfly final at the 2008 Olympics, Phelps remained calm and counted his strokes to victory, winning the gold medal and breaking a world record.

Translating Lessons from the Pool to Financial Preparedness

Just as Michael Phelps prepared for the unexpected by practising what-if scenarios, individuals must be ready for unforeseen challenges in their financial lives. Here are some specific what-if scenarios that everyone should consider:

- What if the market crashes?

- What if I lose my job?

- What if I am diagnosed with a serious illness or have an accident and require extensive medical care?

What if the market crashes?

Imagine you’re an investor, and the stock market crashes tomorrow. What would you do?

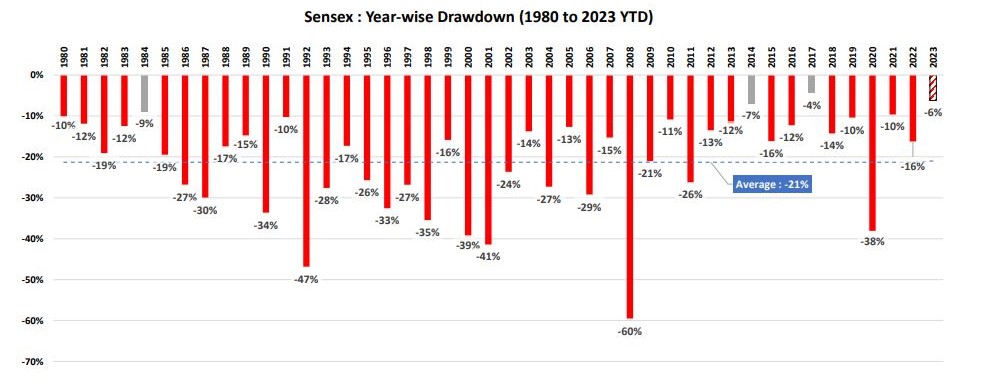

Market crashes are inevitable. Over the past 42 years, the Indian equity market (Sensex) has seen 10-20% declines nearly every year. If you’re prepared, you’re less likely to panic and make impulsive decisions, such as selling your investments at a loss. But if you’re not prepared, you could end up making some costly mistakes.

A fall in the market often presents the best buying opportunities in hindsight.

Here is a simple plan that you can follow:

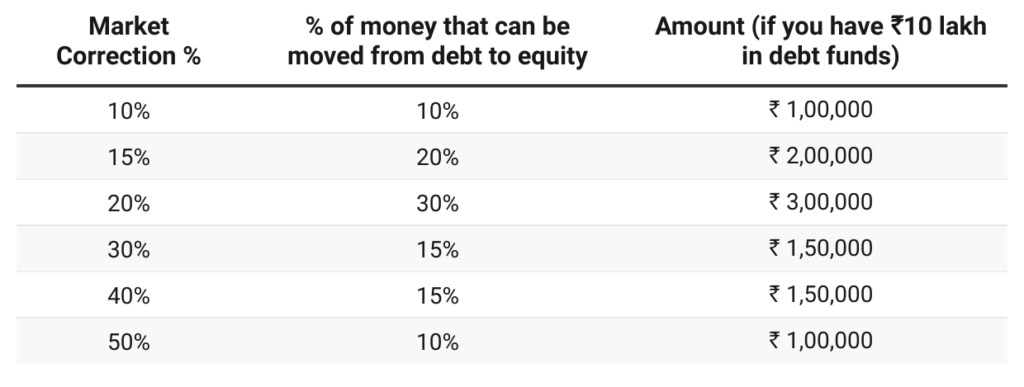

- Allocate a portion of your funds into debt investments, such as debt mutual funds. When the stock market declines, redirect a portion of those funds towards purchasing equity mutual funds at lower prices.

- To illustrate, suppose you have ₹10 lakh invested in debt funds. If the market experiences a 10% dip, consider investing ₹1 lakh in equity funds. If the market correction deepens to a 15% dip, you may invest ₹2 lakh in equity funds, and so on.

- This strategy allows you to acquire stocks at reduced prices during market downturns, potentially enhancing your long-term returns.

What if you lose your job

If you lose your job, it is important to have an emergency fund in place to cover your expenses until you find a new one. Aim to have an emergency fund that is equal to at least 3-6 months of your living expenses.

You might also want to think about investing in assets that are not closely correlated to the stock market. This could include fixed deposits and debt mutual funds. This will help to diversify your portfolio and reduce your risk.

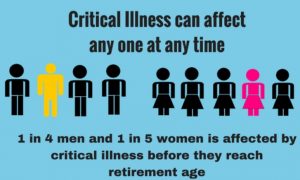

What if you are diagnosed with a serious illness or have an accident and require extensive medical care?

Make sure you have comprehensive health insurance in place to cover your medical expenses, especially if you are self-employed or frequently change jobs. Employer-provided health insurance often offer limited coverage, typically ₹3-5 lakhs, with co-pay requirements.

Having separate medical insurance can offer peace of mind, ensuring protection for you and your family during career changes. Once you have a medical insurance cover in place, you can consider taking out a critical illness and accident insurance policy. This type of policy can provide you with a financial payout if you are diagnosed with a critical illness or have an accident.

Prepare for your biggest what-ifs and train for your financial success.

Just like Michael Phelps, you can overcome any challenge if you are prepared. Start by thinking about your biggest what-ifs. What are your financial fears? Start developing a plan to overcome the challenges you’re worried about.

By considering what-if scenarios and developing a plan for each one, you can reduce your stress and anxiety, and focus on your long-term financial goals.