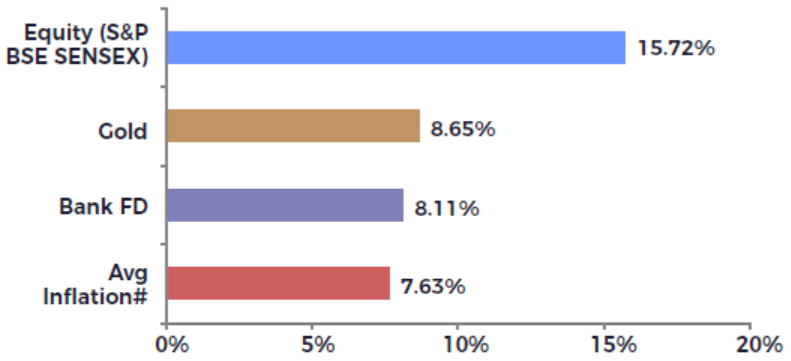

SENSEX has delivered a compound annual growth rate of 15.72% between March 1979 (its inception) and March 2021. This is approximately 8% higher than the average inflation rate during that period.

So should we invest all our savings in equity? Certainly not.

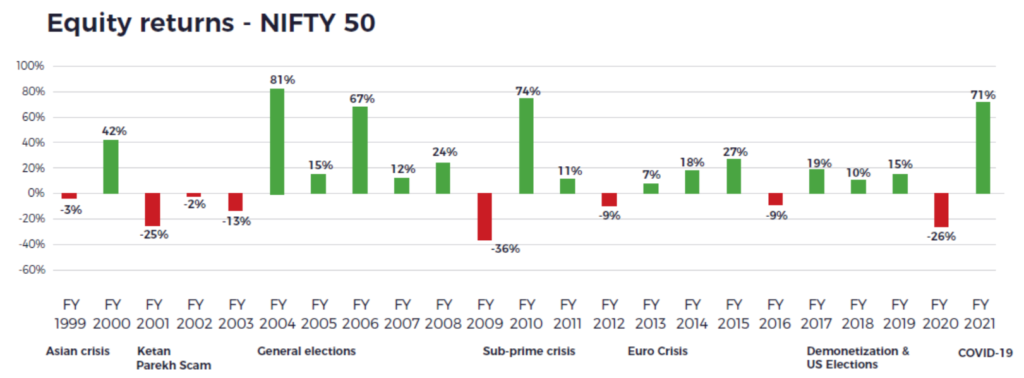

Equity markets don’t rise in a linear fashion. A wide variety of national and international events drive the market in the short run. In the long term, however, returns usually align with the growth of our economy.

As seen in the chart below, markets have delivered positive returns in some years and negative in others. Despite the volatility in the short term, equity as an asset class has outperformed others over the long term.

Only if you can weather short term volatility, will you be able to remain invested in the long term. How can you stay invested for the long term to benefit from equity returns?

Survival

The ability to stick around for a long time without being forced to give up makes the biggest difference. This should be the cornerstone of your strategy; whether in investing, in your career or in your business.

Compounding delivers impressive results only after you give your equity investments time to grow for years and years.

Be Financially Unbreakable

Being “financially unbreakable” is a more desirable objective than “chasing maximum returns”. If I’m unbreakable I am more likely to bag the biggest returns, because I’ll be able to hold on long enough for compounding to work wonders.

Everyone wants to invest during a bull market. They want to own assets that appreciate big time. Say debt funds or FDs earn 5% and stocks generate 12% annual returns. That 7% gap will persistently nag at you.

If debt funds or fixed income products prevent you from having to sell your stocks during a bear market, they are priceless. Because preventing one desperate, ill-timed equity sale, can boost your lifetime returns more than picking a handful of big-time winners.

Avoid extremes. Never go all in or all out. Both are highly risky behaviour usually accompanied by poor research and impulsiveness, leading to erratic outcomes. It’s one thing to say, “drat, I don’t think I can handle a portfolio of 80% equity, I’ll dial it back to 60%.” It’s an entirely different matter to say, “I can’t handle the volatility. I’m going to liquidate until things settle down.” One person is going to make it through the ups and the downs and the other person isn’t. Let’s look at a solution to this problem: EPF.

Employee Provident Fund

EPF is a mandatory government scheme in which retirement benefits are accumulated. The interest rate on the EPF is declared annually. It is currently 8.1%, a nice fat chunk of a return given the current interest rate scenario.

Why Contribute Towards EPF

Your money is safe. The EPF scheme comes with a sovereign guarantee. So there is zero risk of default.

EPF is tax exempt at all levels – at the time of investment, on interest accrued and at the time of redemption. First, Section 80C of the Income Tax Act allows investments in EPF to be deducted up to a maximum of Rs. 1,50,000. Second, the interest earned is tax-free. Third, proceeds on withdrawal are tax-free as well. This makes its returns higher than the post tax returns of bank deposits or other small savings schemes.

Your EPF corpus cannot be used by ourts to repay your loans. For loan defaulters, banks use an attachment order by the court to claim assets such as land, shares and mutual funds to repay. Once assets are attached they can’t be used or sold. The Govt of India has placed the Provident Fund under special legal protection so it can’t be attached by any Indian court.

EPF Interest Rate Down To 8.1%, Should I Invest?

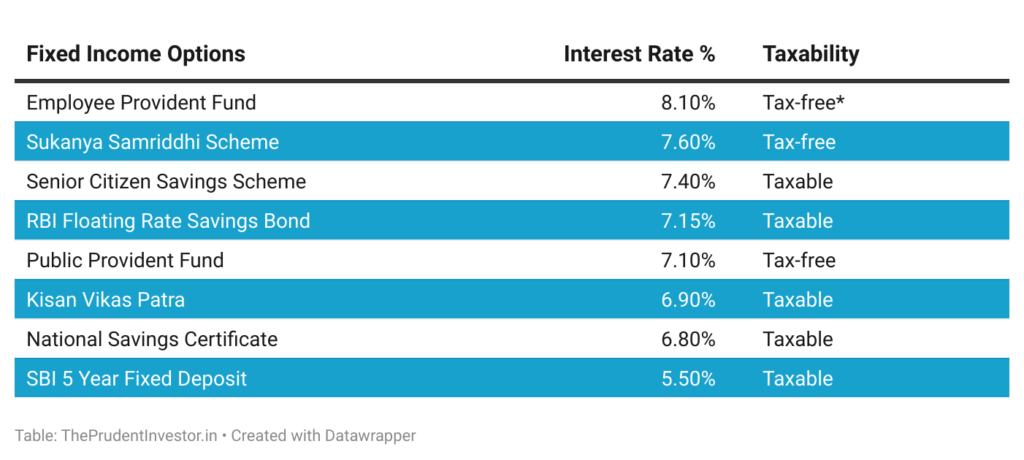

Even after the rate cut, the EPF interest rate is higher than what comparable fixed income instruments offer.

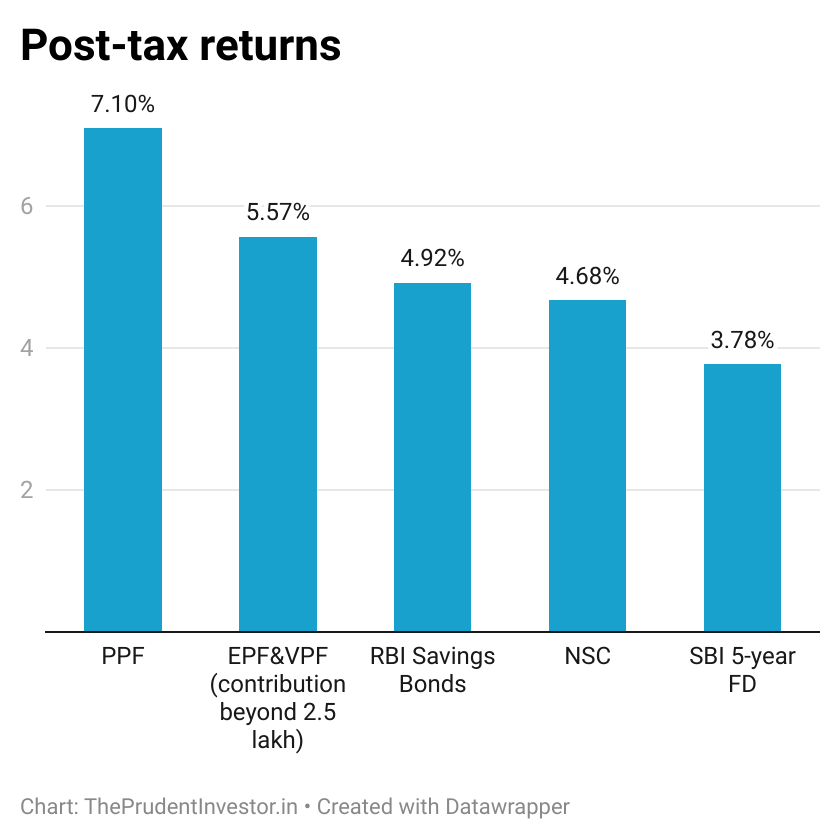

As seen in the table above, EPF offers the highest returns among government provided Fixed Income options. So if you aren’t exhausting the 2.5 lakh limit then you may want to invest further through the Voluntary Provident Fund.

Voluntary Provident Fund

VPF is an extension of the Employees’ Provident Fund (EPF). Only individuals who have an active EPF account and regularly contribute towards EPF can invest in VPF. VPF is voluntary and is over and above EPF which is statutory.

An employee can contribute the entire basic component of their salary to VPF. From 1st April 2021, interest on contributions more than Rs 2.5 lakh per annum will be taxed. For investors in high tax brackets, this lowers post-tax returns.

For instance, a person earning a monthly basic pay of Rs 100,000 (Rs 12 lakh a year) will contribute Rs 120,000 a year to the EPF. He can additionally contribute up to Rs 1,30,000 in the EPF account by putting Rs 10000 every month via the VPF.

Before bingeing on VPF, remember that contributions exceeding Rs 2.5 lakhs will be taxed yielding post tax returns of 5.57% (assuming a tax bracket of 30%). In this case it is advisable to invest any additional contribution in PPF.

While VPF is only for salaried employees, PPF is for both salaried and non-salaried individuals.

Unlike other post office schemes however, the interest rates in EPF and PPF are not locked at the prevailing interest rates for the entire tenure of the scheme. So if the government were to cut rates anytime soon, the new rates will apply to your entire PPF balance.

Individuals who come in the higher income bracket can invest in both VPF and PPF to avail tax-free interest to a certain extent.

Investing in safer, sovereign guaranteed products providing decent returns helps the investor to stomach the volatility equity presents in the short term. This increases the likelihood of the investor staying for the long haul and reaping the double digit returns equity delivers in the long term.

Securing a strong defence allows you to attempt a strong offence. Once you know that the foundation is in place, you’re free to take bolder risks.