The stock market is at an all-time high and there is chatter of a market correction. However, are you doing anything to shield your portfolio in anticipation of a correction? Like rebalancing your portfolio?

Many investors don’t proactively safeguard their portfolios. Sadly, one of the consequences of a bull market is investor complacency. Since a market correction is inevitable, periodic rebalancing is generally a good way to keep your portfolio within risk tolerance.

What Is Rebalancing?

Rebalancing is the process of buying and selling portions of your portfolio in order to set the proportion of each asset class back to its original allocation. If an investor’s risk tolerance or investment strategy has changed, they can use rebalancing to adjust the ratios of each asset class to fulfill a newly desired plan.

Blown Out of Proportion

Portfolios naturally get out of balance as the prices of individual investments fluctuate over time. Therefore, the percentage that you have allocated to different asset classes will change. This may increase or decrease the risk level of your portfolio. Let us compare a rebalanced portfolio to one in which changes were ignored, and then we will look at the potential consequences of neglected allocations in a portfolio.

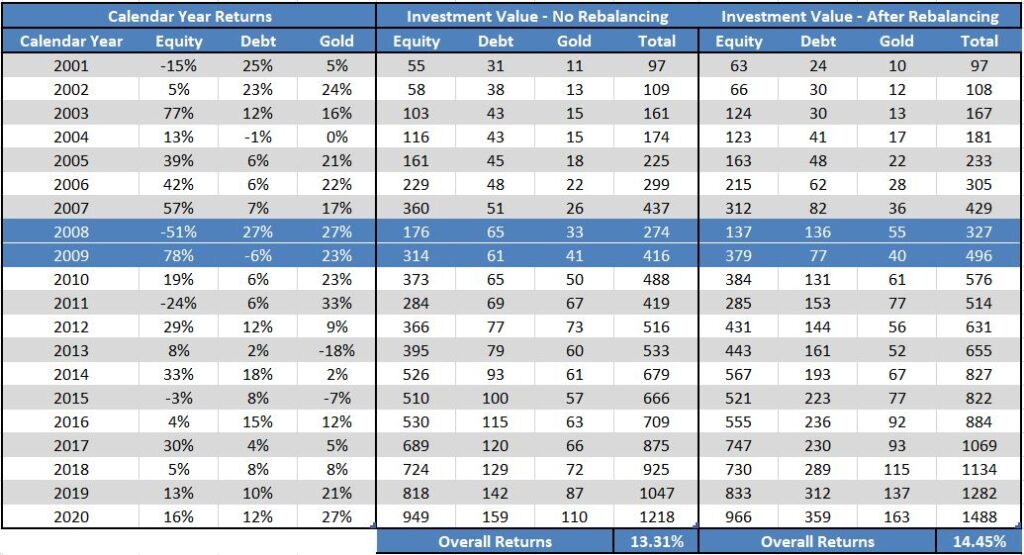

Let us take the example of Rs 100 invested at the beginning of 2001, which was split with Rs 65 in Equity, Rs 25 in Debt and Rs 10 in Gold.

What needs to be emphasized is the changes during 2008 and 2009. The stock markets had crashed in 2008, only to rally massively the next year. A portfolio rebalanced on 31st December 2007 would have started with lower equity and a higher debt proportion; which in hindsight, would have been advantageous because in 2008, not only did equities fall by 51% but the long-term debt portfolios grew by 27% due to the sudden fall in interest rates.

Further, you would have benefitted in 2009 as well, when the equities grew by 76% while bond returns fell by 12%. Thanks to rebalancing, your investment portfolio would have taken complete advantage of equity’s fall in 2008 by stacking more in equity at the end of 2008, and a lower amount in debt.

If you did this rebalancing annually till 2020, your Rs 100 would have grown to a plump Rs 1488 by 2020 yearend, earning a return of 14.45%. Without rebalancing, your portfolio would be much lower at Rs 1218, delivering an average 13.31% return.

It is a human tendency to believe that if an investment has performed well in the recent past, it will perform well in the near future as well. Sadly, past performance is not always an indication of future performance. Many investors, however, remain heavily invested in last year’s high performing asset class and may lower their exposure in last year’s low-performing asset class, which will alter the original allocation.

How To Rebalance

Rebalancing can be achieved in two ways:

1, Sell holdings in asset classes where the portfolio is overallocated and invest the proceeds in underweight asset classes.

2, Allocate new money strategically. For example, if one asset class has become overweight in your portfolio, invest your new inflows into the underweight asset class until your portfolio is balanced again.

Please note: Rebalancing is not intended to increase your long-term returns. Rather, the purpose of rebalancing is to manage risk. It’s a way to keep your portfolio in line with your risk appetite.

When To Rebalance?

Threshold-linked: Rebalancing is done when the actual asset allocation varies from the desired asset allocation by an earlier decided percentage, For example, if you decide your want your equity allocation to be 60% and thanks to a bull run, it is now 70%, it is time for rebalancing.

Time-linked: Rebalancing is carried out at regular intervals: semi-annually or annually.

Time-and-threshold-linked: The portfolio is observed as per schedule but rebalanced only if the actual allocation varies from the desired allocation by the earlier decided percentage.

Exceptions: Major Life Changes or Sudden Cash Inflow like retirement, a baby on the way, buying a house, a major health event or an inheritance.

Advantages of Rebalancing

1, Maintaining Your Desired Asset Allocation And Risk Tolerance

As mentioned earlier, the purpose of rebalancing isn’t to beat the market, it is to manage risk. Your asset allocation determines your risk appetite as an investor. While it may be tempting to “let your winners ride” during a bull market, a prolonged overallocation to equity can result in outsized losses during the next correction.

2, Buying Low And Selling High

This is the objective of all investors. Rebalancing inherently directs investors to book profits periodically and stock up on the asset class which is underweight.

3, Sticking To A Rules-Based Approach

Money is an inherently emotional matter. Having a rational methodology for investing helps keep our emotions in check. Rebalancing is one such practice. Establishing a balanced portfolio and taking steps to keep it that way can help you to avoid relying too much on emotions when making important investment decisions.

4, Fear and FOMO

As will inevitably happen, fear grips us when the markets are heading southward and we might sell low. We also experience FOMO (fear of missing out) at that “hot opportunity” everyone is talking about. The commitment to rebalancing helps to prevent us from acting rashly.

Drawbacks Of Rebalancing

1, Sacrificing Returns For Risk Management

In the long-term equity delivers higher returns than debt. But rebalancing might involve selling equity and buying debt. This might be a price we pay for a more stable and secure portfolio.

2, Transaction Fees

The buying and selling involved during rebalancing incur transaction fees. This is why it might be preferable to rebalance with new fund inflows versus buying and selling current investments.

3, Taxes

While nobody likes to pay more taxes than necessary, it might be preferable to pay some extra taxes on investment gains than to experience significant losses during the next market correction.

If you’re one of many investors who don’t rebalance, you may be better off investing in dynamic asset allocation funds so as to benefit from drastic changes in asset prices in volatile times. Corrections are an inevitable part of being a long-term investor. Thinking that this time is different always ends badly.

Over the long term, a buy-and-hold strategy with no rebalancing usually outperforms since equity tends to outperform over most long-term periods. So why on earth are we advocating rebalancing? Because a buy-and-hold strategy on average is more volatile than a rebalancing strategy as the proportion invested in equity exceeds the original target.

When you have a smoother ride, you’re more likely to stay invested. And staying invested is crucial to realizing returns. Investors who stay the course come out ahead, while those whose portfolios encounter extreme volatility tend to buy and sell at the wrong time. Thereby, they often don’t meet their financial goals.

Rebalancing a portfolio advocates the “sell high, buy low” investment rule – taking the gains from high-performing investments and reinvesting them in those that are yet to experience notable growth. Rebalancing is about keeping risk at tolerable levels not maximizing returns.