Sidharth was enjoying playing cricket with his four-year-old son, Laksh. He couldn’t believe how time was flying. First his marriage in 2014 and the birth of Laksh in 2017. He thought about his journey from husband to father. He also thought about the change in his financial responsibilities.

Sidharth considered the new home they purchased on loan, Laksh’s higher education, his wedding, and what about the effect of inflation on all these. Before he got married, he had a term insurance (aka life insurance) of 1 crore which he doubled to 2 crores a short while after he got married. Looking at Laksh growing bigger, Sidharth feels it is time for another increment in his term insurance. Probably to 3 crores.

“Oh no! I’ll have to go for medical tests again! Isn’t there a better way to do this?” Sidharth thought to himself.

What is Term Insurance

Term covers are the most basic form of life insurance that pay up the sum assured if the insured passes away during the term of the policy. If the insured person survives the term, there is no payment.

Say a 30 year old person has a term insurance policy of Rs. 1 crore with a policy term of 40 years. If the policyholder passes away before the end of the policy term, the entire Rs 1 crore will be paid to his nominee.

It is one of the most effective ways to protect people who are financially dependent on you from an unforeseen event, and buying a policy is cost-efficient. The policy offers a considerable life cover at a small premium.

Insurance companies also offer “return of premium” life insurance. As the name suggests, premium payments are returned after the term expires if the policyholder is still alive. However one should avoid these kinds of policies. To find out why, you can explore our previous article: Return of Premium Insurance Policy: a Godsend or a Ploy.

Who should buy Term Insurance

To answer concisely, anyone earning an income and with financial dependents. As time passes, the dependencies in our lives might increase too. Some have their partner and children while others have their parents to support financially. It is our responsibility to secure their future in the event of an untimely demise.

How Much Term Life Insurance Do I Need?

Just buying life insurance is not enough. The key is to get an adequate sum assured to take care of your family’s current lifestyle in the long term. But how much is enough?

For this we need to consider our day-to-day household expenses, loans and goals such as children’s education and taking care of financially dependent parents. The figure you reach is the total money that your family will need.

The next step is to deduct the present value of your investments and life cover you already have. The figure you get by deducting investments and insurance cover from expenses and goals will give you an idea how much cover you need.

The Need for Growing Term Insurance Cover

As you acquire family and it expands with children, so do the responsibilities of providing them a secure financial future. Therefore, your insurance cover, especially the term insurance cover should also grow.

How can One Increase Term Insurance Cover?

There are several ways you can increase your term insurance cover to match your growing responsibilities:

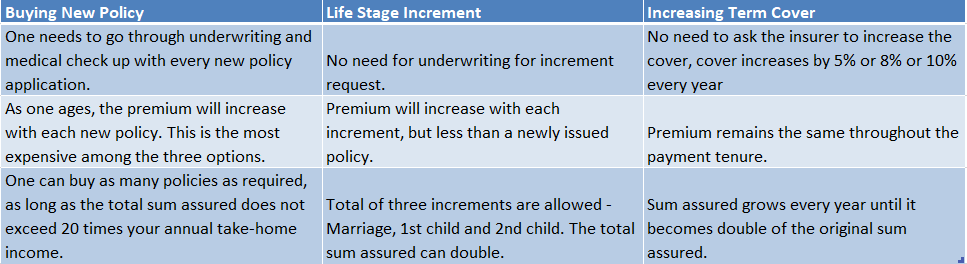

- Buy additional life covers: Buying additional life cover is straightforward as you can apply for a new term or other life insurance policy with significant growths in your income.

- Buy a plan with Life-stage increment options: You can ask the insurer to increase your sum assured of the policy at specific predefined points in life. However, the policy should have this option at the time of purchase.

- Get an increasing cover term insurance: Increasing term cover is where your sum assured of the plan automatically increases every year. Here as well, you do not need to buy another policy; you won’t even have to submit a request for increment.

What Are The Differences?

When to Select Which?

There are several considerations to keep in mind about these three options:

- New Policies: If you didn’t choose Life-stage Growth or Increasing Term Cover at the time of buying your policy and you realize later on, say when you purchase a house on loan, or after marriage or the arrival of a child that you want to increase your cover: This is the only option available.

- Life-stage Growth: This is an option for those buying early or at least right after marriage. As the largest increment occurs at marriage (50%), it makes sense to have this option in the policy if you are buying before marriage.

- Increasing Term Cover: This is the most convenient cover. The sum assured can keep growing automatically every year as your life goes on. If you already have a family, this might be a preferable choice for you.

New Avatar of Term Insurance: Increasing Cover Option

One of the latest additions in the features of term insurance plans is the growing term insurance plans. These plans offer you the choice to increase the benefit amount without buying a new policy each time.

In an increasing term insurance plan, the sum assured increases every year by a specified percentage. Unlike a regular term insurance plan, an increasing term plan increases the sum assured during the policy period.

Even though the term insurance cover increases every year, the premium remains the same throughout the policy term.

Benefits of Increasing Term Life Insurance

Covers Rising Costs

Life gets more expensive as one ages. You will probably need more coverage in the future than you do currently. If you intend to start a family or purchase a bigger house down the road, increasing term life insurance can be beneficial.

Inflation Protection

The value of money decreases over time. Purchasing a 30-year term cover of Rs 1 crore today will not be as valuable in the future. Considering an inflation of 5%, the present value of 1 crore will be around 25 lakhs. An increasing term protects against inflation by increasing the death benefit over time.

Affordable

The major advantage of purchasing an increasing term insurance policy is that it offers a very reasonable premium. More importantly, the premium of the policy also remains the same throughout the policy tenure and doesn’t rise with the incremental sum assured.

No Additional Underwriting

Increasing term insurance allows you to increase your coverage in the future without reapplying to the insurer or undergoing a new medical exam.

One premium

With a traditional upgrade, you purchase a new policy by paying an additional premium which will depend on your age and your health status at that time. Throughout the term, you will have to pay two premiums. Meanwhile with an increasing cover, you will only have a single policy and a single premium, lifelong.

Automatic increase

When you upgrade manually, you’ll need to submit documents, sign new declarations, and undergo new medical tests, etc. in addition, there could be additional terms and conditions that will be applicable too. But with increasing covers, no new forms, documents, declarations or medical tests will be required.

No risk of rejection

If you decide to manually upgrade your policy when you’re older, there is a chance that you’ll have to pay hefty additional premiums due to a higher age and any medical condition or disease you get over the years. There is also the risk of the proposal being rejected due to higher age or poor health. But with increasing covers, you won’t have to worry about paying additional premiums or the policy getting rejected.

Tax Benefits

With Term Insurance plans you can avail tax benefits on premiums paid under Section 80C of the Income Tax Act, 1961. You can avail tax benefits up to Rs.1.5 lakh on the premium paid.

How are increasing covers priced?

If you compare the initial premiums, you’ll notice that a regular, non-increasing cover has more inexpensive premiums compared to those of an increasing cover. But let’s look at the total cost involved over the duration of the plan. Let’s understand this better with an example.

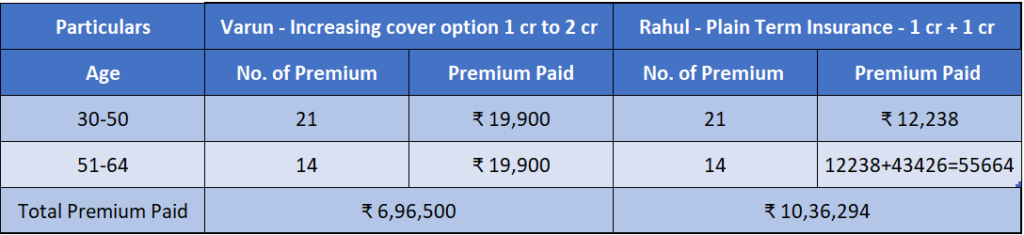

Rahul a 30 year old non-smoker takes a cover of 1 cr at the age of 30, which has a premium of Rs 12238.

Varun, his twin brother, also a non-smoker, opts for 1 cr increasing cover option with 5% cover increase per year and pays a premium of Rs 19900.

Fast forward 20 years, Varun’s cover has now increased to 2 cr and Rahul thinks he should also increase his cover by another 1 cr and this new policy has a premium of Rs. 43426.

Over a 34-year period, Rahul pays Rs 3,39,794 more than Varun as the premiums increase steeply with age and health conditions.

Overall, you can understand how choosing the increasing cover option while buying term insurance is superior for uncomplicated management of your term insurance plan, as well as straightforward management of the claim by your family.

It is hassle-free, automatic and doesn’t require you to go through any medical tests or submit any new documentation.

All this while ensuring that your family has sufficient cover throughout the policy term.

An increasing term insurance plan is a excellent choice for financial security whether you are a young working professional, self-employed or business owner. It helps you to plan for growing responsibilities and increasing liabilities in advance and beat inflation.

We highly recommend that you choose an increasing cover option when buying term insurance plan.