In my early twenties, I invested 20,000/- into four specific stocks. I would check the price of each stock daily, sometimes numerous times in a day.

When the price went up, I was happy high and when it went down I was low.

Back then I had the feeling I was doing a great job of keeping track of my minuscule investments. The big thing I missed on was that I didn’t invest enough for the gains to actually make an impact to my finances.

Let’s suppose I earned a 20% returns on my stocks in one year, that amounts to 4,000/-. Though the ROI is significant, the amount is not life changing. Looking at the big picture, 4,000/- is a negligible amount.

So what’s the point of it all? The point is the amount invested matters more than earning a phenomenal return over an average return. It feels fantastic to earn double digit returns but on a very small portion of your total wealth, it is not going to make you rich.

Your Savings Rate Is Important

At the beginning of your investment journey, how much of your earnings you save has a considerable impact on how soon you will achieve your financial objectives.

How do we calculate your savings rate? We divide your total savings (funds put into savings and investment accounts) by your total income (if you are salaried, then your take home). For example, if your annual income was 20 Lakhs and you saved 6 lakhs this past year then your savings rate is 30%.

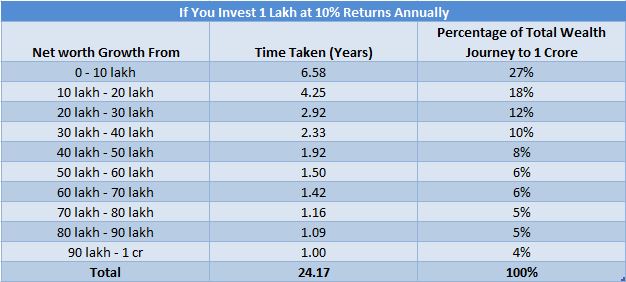

What difference does it make? Let’s say you invest 1 lakh annually at an average rate of return of 10%. To build a corpus of 1 crore it will take you 24 years. What is worth noting is that to earn your first 10 Lakhs (10% of your total corpus) it will take you 6.58 years, approximately 27% of your total duration to 1 crore.

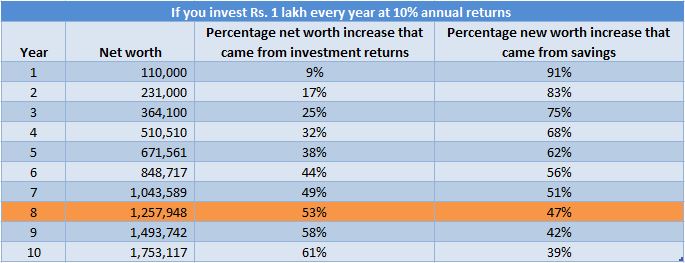

You’re saving the exact same amount every year, but your past savings are working hard to increase your net worth more at a faster rate every year. This is the power of compounding.

Observe this astonishing statistic: To go from 0 to 10 lakhs, it takes 6.58 years but to go from 60 lakhs to 1 crore take less time than that; it takes 4.67 years.

This just goes to show how immensely potent compound interest is once you’ve saved 20-30 Lakhs. Once you pass a certain limit, your savings work harder than you do. It’s like rolling a snowball from the top of a hill. Time and a high savings rate are your leverage and fulcrum.

When you’re just beginning to invest, the amount you save has a far greater impact than your rate of return.

Compound interest requires time to grow. Towards the beginning, there isn’t enough money invested for the returns to seem to matter. It takes a good 8 years for the returns to surpass savings in contributing to net worth.

When you not only save but invest your money, it earns money of its own. The money earned earns money all but itself. Over time, this becomes an exponential escalation of wealth.

Once your returns are enough to pay for your expenses and leave enough returns invested annually to match inflation, you can gleefully retire.

In the first year, you earned only 10K as returns. Your intial savings of 1 lakh contributed 9% of your overall growth. But in the 8th year, investment returns surpass savings as the largest contributor to your wealth.

As you embark your financial journey, you will find out that the first 10 Lakhs can take the longest to accumulate. Of course, hiking your savings rate helps significantly, enabling you to achieve your objectives sooner. As Charlie Munger said:

“The first $100,000 is a b*tch, but you gotta do it.”

When Do Percentages Actually Matter

Many clients and friends try to create a Michael Schumacher portfolio with the objective of delivering fantastic, outperforming returns. They might invest in Bitcoin or research tediously to find complex algorithms to outperform the market by a few percent. Or worse, they might try the impossible; to time the market.

What we didn’t realize as beginners was that initially the amount invested was so small, the rate of return didn’t make a world of a difference. My 20% returns on my 20,000/- investment back in the day earned me only 4,000/-.

The magic was that I learnt to save a large portion of my earnings and invest it which has paid me handsomely today. I was naïve to believe that my returns were going to make me rich that early.

In the initial stages, your wealth creation will come from accumulation. That is, your savings and not your returns. But that will change. After a decade or so, the tortoise of investment returns beats the hare of savings.

A 10% return on 10 Lakhs is 1 Lakh.

A 10% return on 50 Lakhs is 5 Lakhs.

A 10% return on 1 crore is 10 Lakhs.

Focus on Income In The Beginning

My nephew recently asked me for investment advice and I told him the same thing I tell my investors.

Make your investments automatic and;

Utilize your intelligence and effort to increase your income since that is what will count initially.

Pingback: Why Your Savings Rates Matters More Than Your Returns? : The Prudent Investor - FinMedium

Excellent insight , very interesting we all must to be start to invest earlier do patient well follow do this long term gain. Thanks lot prudentinvestor to bring this motivative script with us

awesome

awesome