The 2023 budget brought with it a revamped income tax regime, giving taxpayers the option to choose between the old and new regimes. While the old regime offers more deductions and exemptions, the new regime boasts lower tax rates. Choosing between the two regimes can be a complex decision that depends on your income level and the total deductions you claim.

If you’re a salaried individual, chances are you must have received an email from your HR or payroll team asking you to select your income tax regime for the financial year. If you fail to make a choice, the new tax regime will be set as default and can only be changed when filing your tax returns.

Here’s how the old tax regime differs from the new and what you must choose as a taxpayer.

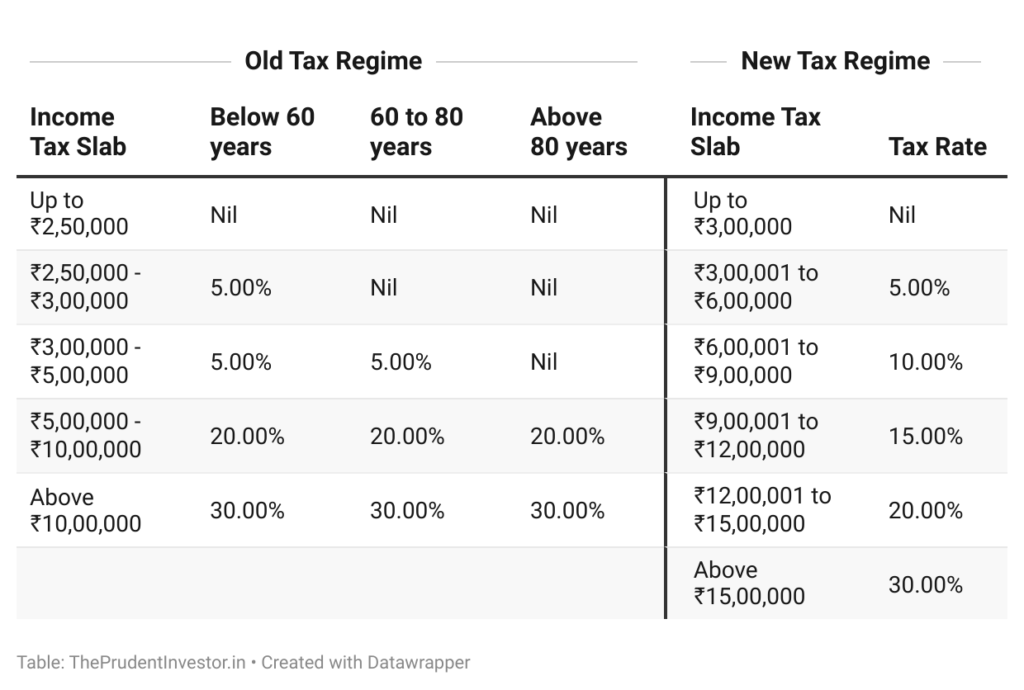

Lower Tax Rates

The new regime has seven tax slabs ranging from 0% to 30%, with the highest tax rate applicable on income above INR 15 lakh. On the other hand, the old regime, offers over 70 exemptions and deductions, including popular ones like HRA, LTA, and Section 80C. Taxpayers can choose which regime works better for their specific financial situation.

Higher Tax Rebate Limit

Full tax rebate on an income up to ₹7 lakhs has been introduced. Whereas, this threshold is ₹5 lakhs under the old tax regime. This means that taxpayers with an income of up to ₹7 lakhs will not have to pay any tax at all under the new tax regime!

Which Tax Regime is Better?

The answer will depend on your income level and the amount of deduction that you can use. The new tax regime is better for people who are unable to claim various deductions and exemptions under the old tax regime.

But, if you can claim deductions like Section 80C, Section 80D, Section 24(b) and house rent allowance (HRA), help taxpayers bring down their tax outgo under the old tax regime.

The Minimum Deduction to Save Higher Tax

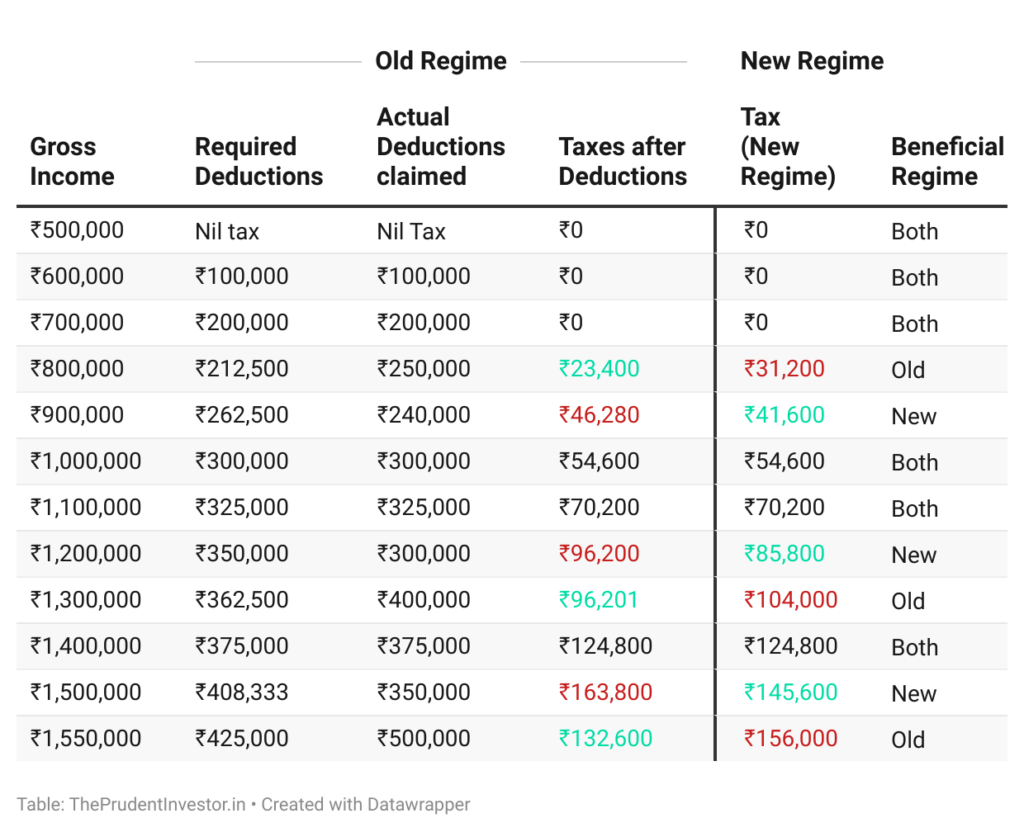

The break-even point between the old and new tax regimes is the income level at which there will be no difference in tax liability between the two options. If your eligible deductions and exemptions under the old regime exceed the break-even threshold for your income level, it’s better to stick with the old regime. But if the break-even threshold is higher than your eligible deductions and exemptions, then it’s advisable to switch to the new regime.

This table compares tax liability under the old and new tax regimes based on an individual’s gross income and actual deductions claimed. The second column, “Required Deductions,” shows the amount of deductions needed to claim under the old tax regime to be at par with the new tax regime.

For those earning between Rs.15,50,000 to Rs.5 crores, if the deductions claimed exceed Rs.4,25,000, the old tax regime will be beneficial. However, beyond Rs.5 crores, the new tax regime is beneficial due to the lower surcharge of 25% compared to 37% in the old tax regime.

Let’s Understand with Examples:

Example 1

- Gross income of ₹10,00,000

- Deductions claimed of ₹3,00,000

- Both Old and New Tax Regime have the same tax liability of ₹54,600

- Either tax regime can be chosen as per preference

Example 2:

- Gross income of ₹15,50,000

- Deductions claimed of ₹5,00,000

- Opt for Old Tax Regime to save tax

- Tax liability is ₹1,32,600 under Old Tax Regime

- Tax liability is ₹1,56,000 under New Tax Regime

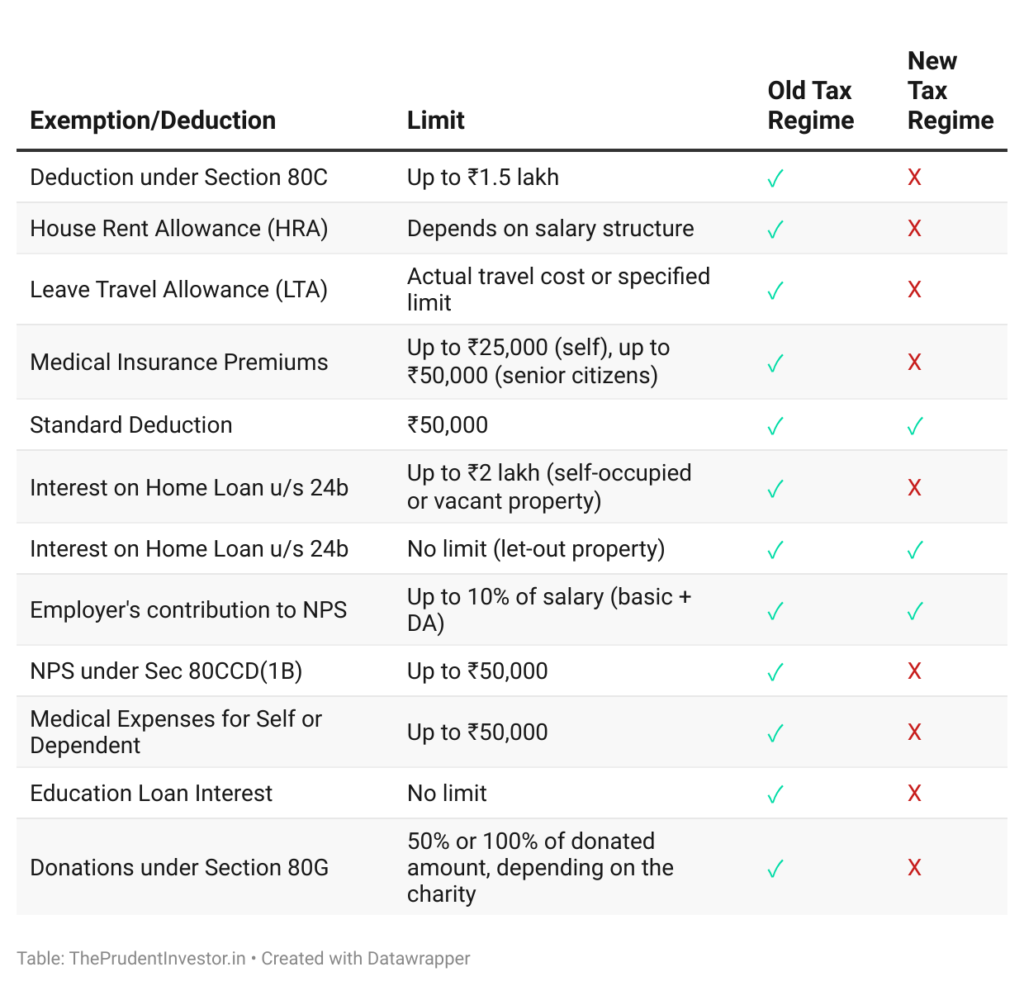

The most commonly used deductions claimed by taxpayers in India

The Income Tax Act, 1961 offers a range of exemptions and deductions that can help lower the taxable income of an individual. But with the introduction of the new tax regime in 2020, taxpayers are now faced with a choice between the old and new tax regimes. To help with this, here is a list of some of the most commonly used deductions claimed by taxpayers in India.

Summing It Up

The old tax regime still looks more lucrative for people with higher annual incomes, but only if they have the investments to claim enough deductions.

However, for individuals who do not want to invest in too many long-term tax-saving schemes or do not have a housing loan, the new income tax regime could be the answer.

High net worth individuals will find the new tax regime beneficial, while people in the middle income brackets who claim multiple deductions could still be better off with the older tax regime.