Virat bought a life insurance policy a couple years ago for tax saving. Now that he pays a big home loan EMI, he finds it difficult to service the 1 lakh insurance premium. He wants to know whether he can redeem his ELSS funds and reinvest the proceeds to claim tax deduction this year.

Santa’s Gift: Section 80C

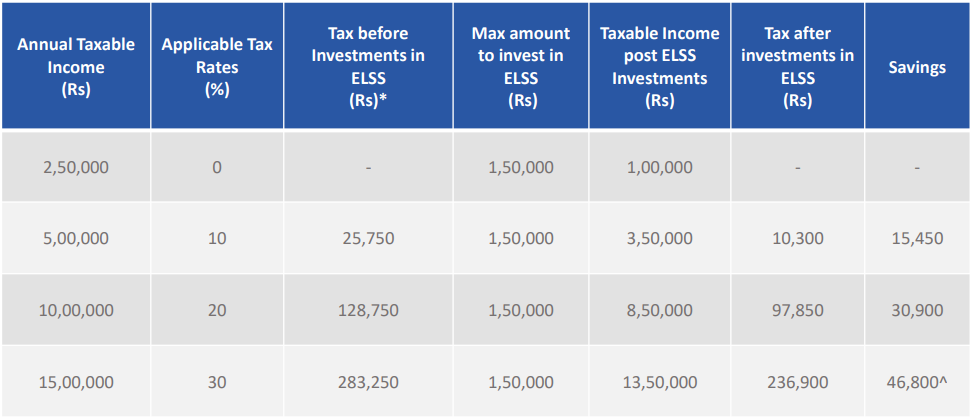

Every financial year, Section 80C offers a window of investment opportunities of up to 1.5 lakh. This benefit is available to everyone, regardless of their income tax slab. So if you are in the highest tax bracket of 30 percent, the investment of 1.5 lakh under this section will save you Rs 46,800 annually. There are a variety of financial products that qualify for these benefits including tax planning mutual funds, also known as Equity-Linked Savings Scheme (ELSS).

The investment that makes the most sense for the majority of tax payers is an ELSS. Salary-earners usually have some of the permitted amount going into fixed income through PF deductions. Equity is advisable to balance that.

What are ELSS Mutual Funds?

An ELSS is like any other mutual fund that invests primarily in the stock market. The only difference is that an ELSS comes with a three-year lock-in, meaning you cannot redeem your investment before three years from the date of purchase.

How do they help save tax?

Investments in ELSS up to a maximum of 1.5 lakh every year qualify for income deductions under section 80C of the Income Tax act. Meaning you can deduct the amount you invest in an ELSS from your total income to reduce your taxable income and, therefore, your taxes.

For example, Rohit, a senior software engineer, has a taxable income of Rs. 12 lakh a year. So he is in the 30% tax bracket. He chooses to invest 1.5 lakh in an ELSS fund. Under 80C of the income tax act, this brings down his taxable income to 10.5 lakh and he saves Rs. 46,800 (31.2% of Rs. 1.5 lakh).

ELSS Mutual Funds Versus Government 80C small savings schemes

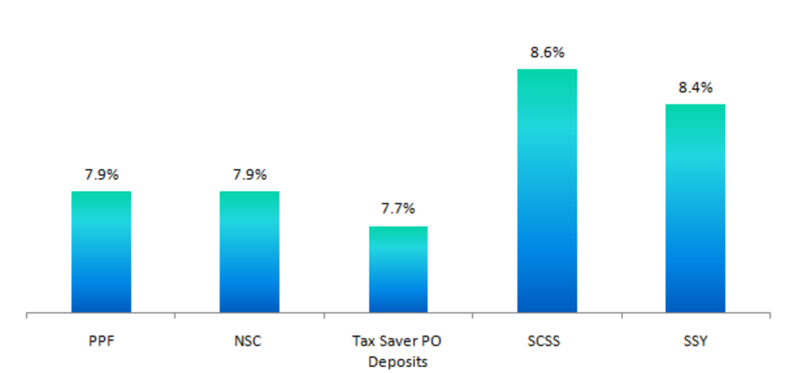

With reference to the chart below, you can see that the interest paid by Government or Post Office Small Savings Schemes is between 7.7 to 7.9%, except for the Senior Citizens Savings Scheme (SCSS) in which only senior citizens can invest and Sukanya Samruddhi Yojana (SSY) in which parents can save for their girl child. Tax payers should note that the interest rates of these schemes are not fixed and are linked to relevant benchmark Government bond yields. Government bond yields have been falling for the past 2 years so the interest rates of these schemes are also following a declining trajectory.

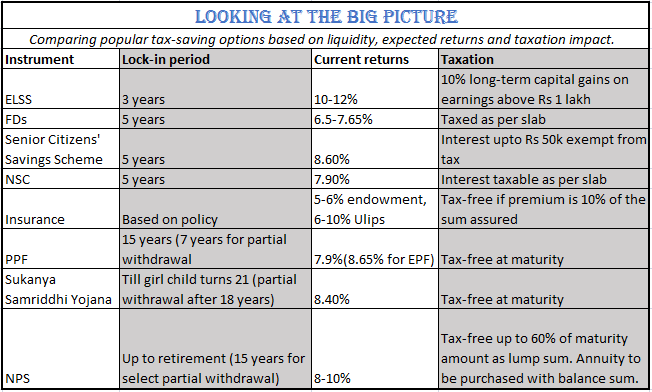

Government or Post Office Small Savings Schemes ensure capital safety, while ELSS mutual funds are subject to market risks. This is because ELSS mutual funds invest in stocks across sectors and various market capitalizations which categorize the stocks as large, mid and small cap. But equities as an asset class have the potential to deliver superior returns in the long term compared to all others. Over the past 10 years, the Nifty 100 TRI (the benchmark index of large cap stocks) has delivered 12% CAGR returns while the PPF gave 8.24% annualized returns in the same period.

Even the worst performing ELSS fund in the past decade has given a return of 8.32% while the best performing fund has given a return of 14.37% with the majority of the funds giving a return of around 11%.

Liquidity

ELSS Funds offer more liquidity than most tax saving investment options. ELSS has a lock-in period of 3 years while other 80C investment options have a minimum lock-in of 5 years. Once the lock-in of three years is over, investors can redeem and reinvest the same money in the fourth year to claim the taxation benefit under Section 80C but they should take Long Term Capital Gains Tax into account.

Tax Advantage

ELSS Funds enjoy a significant tax advantage over many 80C investment schemes. The interest from 80C schemes like bank tax saver FDs, senior citizens savings scheme (SCSS) and national savings certificate (NSC) is taxed as per the income tax slab of the taxpayers (though NSC investors can claim accrued interest during the investment term as deduction from their taxable income). But ELSS capital gains up to Rs 1 Lakh are tax exempt and the capital gains in excess of Rs 1 Lakh are taxed at 10%.