I was recently having a discussion with a client who is a young businessman. I have spoken to him about Goal Based Investing (GBI) before. The goal an investor is saving for could be:

- A vacation house on the beach.

- Perhaps it’s the ability to travel around the world.

- Maybe you want to turn a hobby into a business.

GBI hails from the Bible of Investing as research shows investors stick to their commitments and achieve their objectives with this strategy.

But my client, Rahul, was of the opinion:

“Why should I invest with Goals in mind? I just want to double my money Yaar, the faster the better. How can I plan for retirement and children’s education when I’m not even married. I don’t even have a girlfriend. If the money is there, I can use as and how required. And I have enough to meet my requirements.”

I shared the benefits of GBI with him: Since investors are Human Beings, we are all influenced by Behavioural Psychology. One is more likely to be passionate about 5 Lakhs invested for his son’s education than just 5 Lakhs saved. And less likely to touch that investment for any cause not strong enough.

Rahul felt differently. If I simply have a lot of money (more than enough) I can use it for specific expense as and when they arise. I can divide investments into long term and short term money to optimize my returns.

Rahul’s thought process is not unique. Many consider this question at some point or another. Why should we commit to specific goals? Why not just make money? Good Old Wealth Creation. Well, if this is the ambiguous goal that drives you to save and invest, so be it. Let us set the goal as doubling your money!

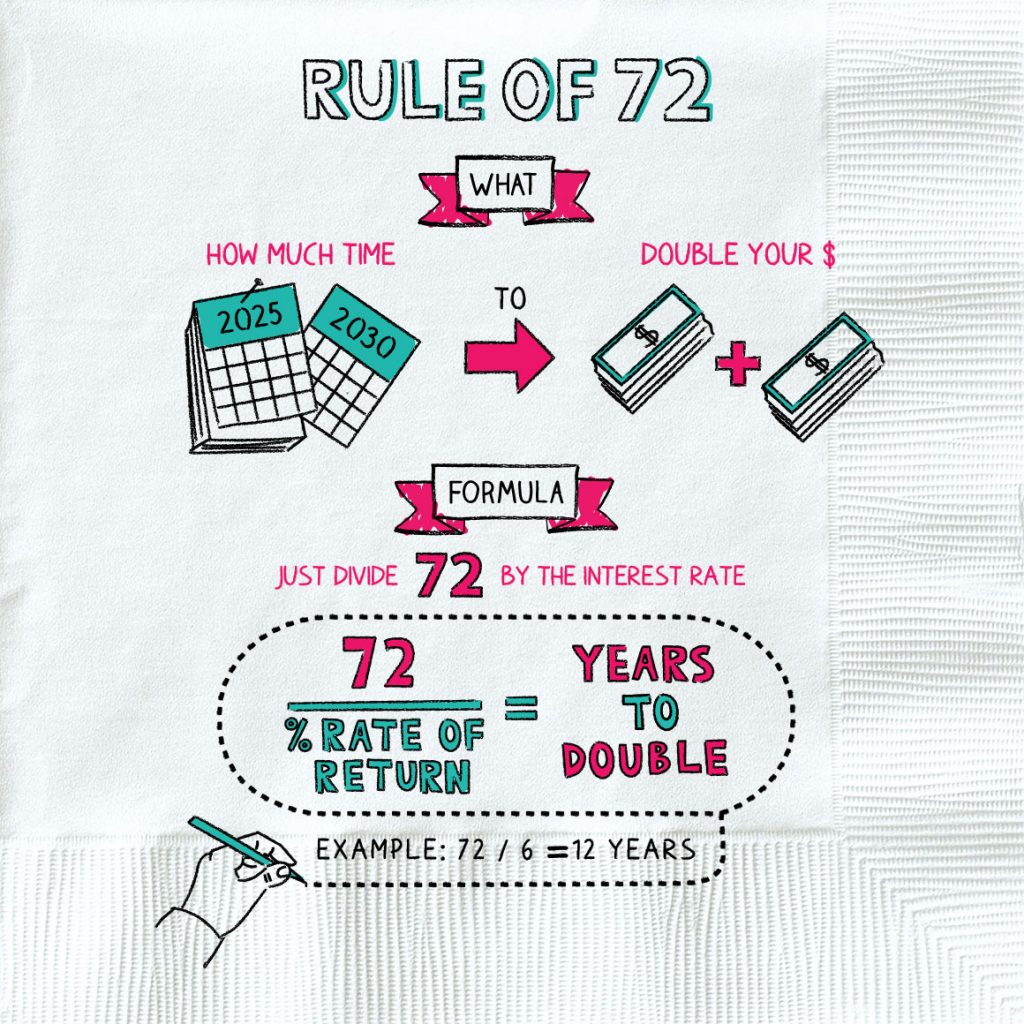

Do you want to know how soon your money will double? The “Rule of 72” approximates how many years it will take. The formula is simple: 72 / interest rate = years to double

For example, if your money earns:

3%, it will take 24 years for your money to double (72 / 3 = 24)

6%, it will take 12 years for your money to double (72 / 6 = 12)

9%, it will take 8 years for your money to double (72 / 9 = 8)

12%, it will take 6 years for your money to double (72 / 12 = 6)

So, if you have put money in an FD which gives 6%, it will take 12 years for the money to double.

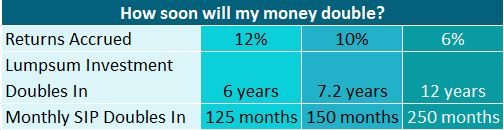

Another option is the Doubling of the SIP. That is, how soon will my SIP double? For example, 20,000/- invested monthly will double in 125 months i.e. Total investment of 20,000/- for 125 months = Rs 25,00,000/- will become a corpus of approximately Rs 50,00,000 at the end of 125th month @ 12% CAGR.

Very often, people who don’t have specific financial goals in place are drawn to endowment policies (insurance products like LIC plans, etc). These have two elements: the amount of investment (inflow) and the amount you receive after a particular period of time (outflow). These products are structured in such a way that stopping too early can lead to very low returns, thereby encouraging the investor to complete all payments and stay for the long run.

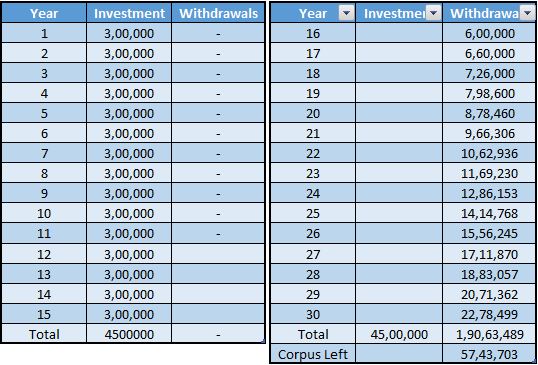

For Example:

Invest 25,000 per month for 15 years.

Withdraw 50,000 per month (Rs 6,00,000 yearly) from the 16th year, increasing by 10% per annum.

For many the “guaranteed assurance” a significantly larger corpus in the later years signs investors up for this product. The unfortunate thing is that, being an insurance product, the investor earns a lower return that if they would have committed to such an amount for that time period in Equity. A beautiful vehicle exists to withdraw in a similar manner: Systematic Withdrawal Plan (SWP).

So any mutual fund can be your “LIC Plan” yielding you higher returns if you practice the same discipline in investing with SIP and withdrawing with SWP. For a better understanding of how you can use SWP for a steady stream of income, read “Wake Up! It’s time to plan your retirement with SWP.”