Vishal Gupta, father of 3-year-old Amaira, wants her to be able to pursue any career of her choice. Without compromising on her dreams for want of funds.

From the moment our child is born, we parents work very sincerely so that our child may dream big without having to think twice about finances and therefore apply ourselves to achieve the same. The aspirations of the current generation of children are bigger and more specific than those of previous generations. We are also a very different generation of parents. We more than support our children to be ambitious and not to settle for less.

High aspirations, however, come at a price.

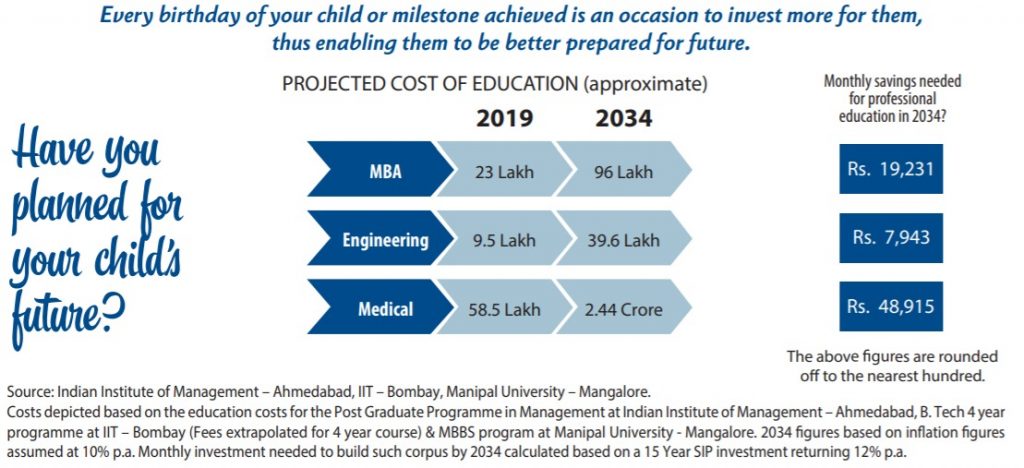

The cost of higher education in India has seen double digit growth (in percentage terms) over the past two decades. The charges for a 4-year engineering degree (B.Tech/B.E) in the premier Government institutes are about Rs 9 – 10 lakhs. At some of the top private institutes, the cost of engineering education can be as high as Rs 15 – 20 lakhs.

The expenditure for a medical degree is similar, if not a little higher. In the decade, assuming an inflation rate of 10%, the cost of engineering or medical education may be between Rs 25 – 45 lakhs. An MBA from one of the premier institutes will expend about Rs 20 lakhs. 10 years from now, you should be prepared to shell out Rs 50 lakhs for your child’s MBA.

While the ever increasing cost of education and weddings due to inflation is beyond our control. We also cannot let our child, with enormous ability and intelligence, forsake his or her aspirations or postpone any plans and settle for less.

Important steps

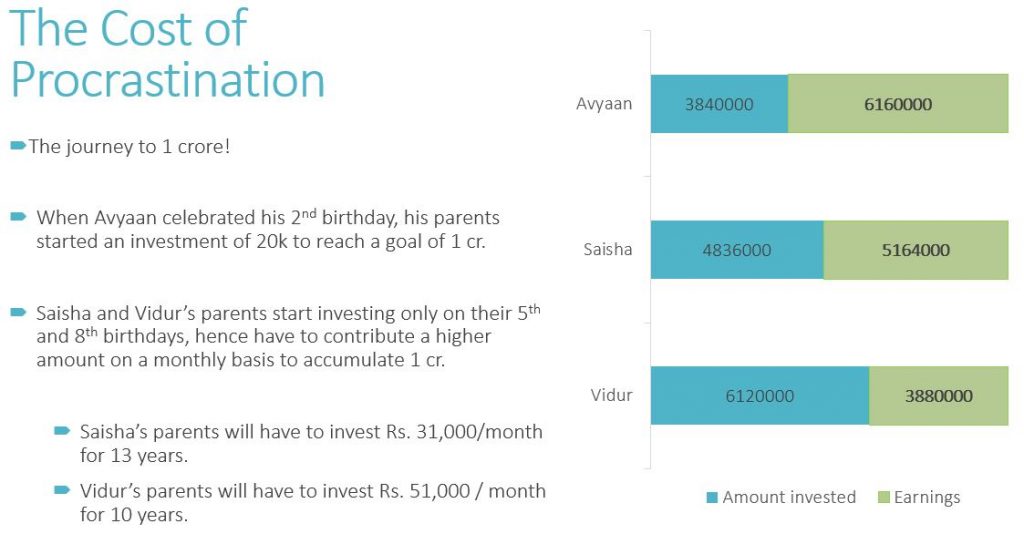

1, With Investing, the earlier the better:

- Relatively, one needs to save less monthly to accumulate the same corpus, assuming everything else being constant. Kindly refer to the table below.

- This gives the money a longer time to compound leading to a larger corpus accumulation.

Unfortunately, we often prolong our investing decidions, even without any strong reasons to do so. We feel a “few months won’t make a big difference.” The reality, however, is that small delays can actually significantly affect the growth of your wealth in the long term. The truth is being rich is not always about making big decision but also small ones like not postponing your SIP and starting the investment journey at the earliest.

2, Do not allow yourself to withdraw now and then:

- For life’s unpredictable emergencies, it may sometimes be necessary to withdraw from funds earmarked for your child.

- This can affect the future prospects of accruing the required amount by the time it is required.

- The solution is to set up distinct funds for various financial goals. One may set up a dedicated retirement fund, travel fund, marriage fund, education fund, emergency fund, medical fund and so on to take advantage of mental accounting and prevent such a situation.

3, Remain invested for the long term.

What are the options?

The cost of education is rising faster than inflation.

Saving is not enough, invest in the right asset!

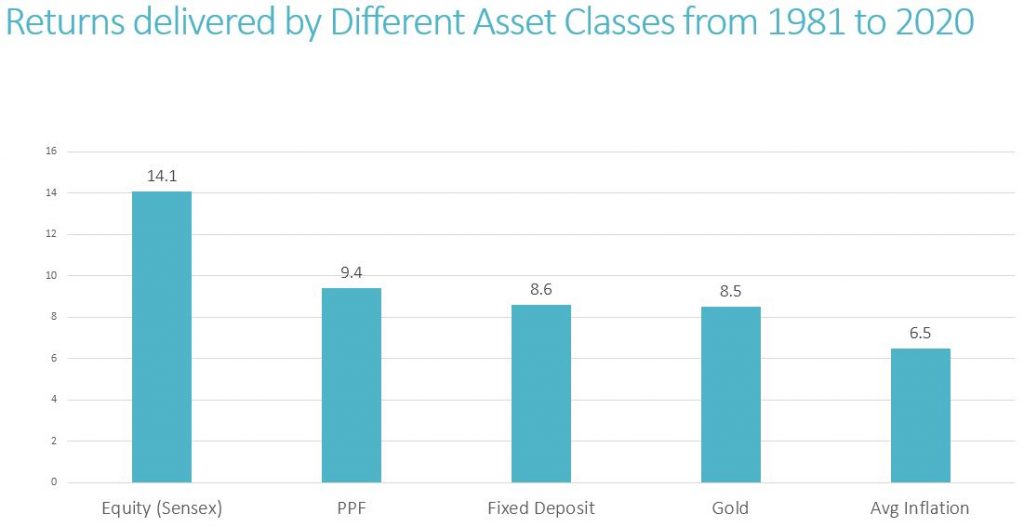

What are the Returns from Different Asset Classes?

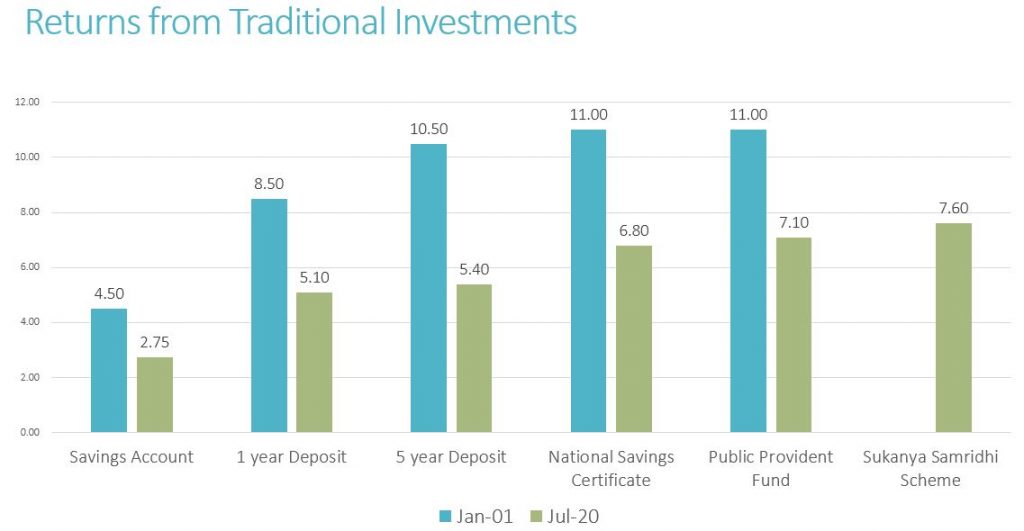

Traditionally, the options for saving for a long term goal were Fixed Deposits and Life Insurance Savings Policies (endowment schemes). The average rate of interest on Fixed Deposits over the past decade is about 7.5%. This is entirely taxable depending on which tax bracket is applicable to the investor. For investors in the 30% tax slab, the average post tax return was about 5.3%.

With endowment policies, whether through Government or Private insurers, the historical internal rate of return was 5-6%. During the building up stage of financial planning, the choice of asset class plays a critical role in determining achievement of the goal. Research has shown that equity is the highest yielding asset class long term investment horizons. In the past decade, the Sensex has provided almost 14% annualized returns.