Gold prices have moved from nearly Rs. 32,000 at the start of the year to close to 38k. After giving a blistering🎇 return of more than 20%, there is a lot of interest in Gold again (No Surprise: India is one of the largest consumers of Gold).

A friend was regretting that he didn’t buy gold when he was in Dubai recently. Another said; “In times of emergency, gold can be pledged to tide over the crisis.”

The ‘Golden🏅question’ here is, how does one invest in gold?

Should you rush to your jeweler💍 and buy that gold necklace you were eyeing for such a long time? Or do gold bars or coins make sense?

Until recently, buying physical gold was the only option. It is, however, an inefficient method of investment.

- Gold jewellery comes with making charges.

- Storing physical gold 🔐 safely also presents a problem for investors.

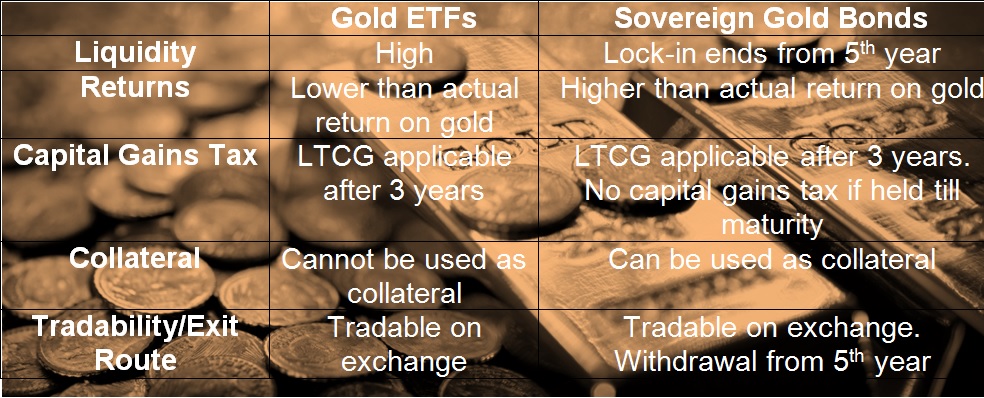

Apart from physical gold, one can buy Sovereign Gold Bonds (SGBs), Gold Funds or Exchange Traded Funds (ETFs). If liquidity is of prime importance then Gold Funds or ETFs are a good option.

Sovereign Gold Bonds deliver better returns than Gold Funds or ETFs because

- No expense ratio in involved in holding SGBs (ETFs charge around 0.35 to 0.8% every year).

- Rather than owning gold in physical form and not earning anything on it, SGBs mean owning gold and also earning interest on it. The government has fixed an interest of 2.50 percent per annum on the investment.

- The big difference is on the taxation front. Gains in SGB on redemption after 8 years are tax-exempt but gains in Gold ETFs after 3 years are subject to 20 percent tax post indexation.

- Most SGBs can be bought at a discount to the actual gold price because as this is not a frequently traded product. There are two sides to this coin: you are getting the discount because there is not much trading volume, so if you sell before maturity you will probably have to sell at a discount as well for this reason.